Short essay · 11 July 2026 · Marcel P.T. Chin-A-Lien · Golden Lane Investments Advisory Group (GLIAG)

1. The macro picture: two records, one message

Last year closed with a clarifying set of numbers.

Global oil demand averaged 105.15 million barrels per day in 2025, up 1.3 mb/d year-on-year, with growth concentrated in non-OECD Asia, Africa, Latin America and the Middle East (Anadolu Agency / OPEC).

Oil remained indispensable — but it also remained politically fragile, trading in a soft USD 60–65/bbl band despite live conflict risk in the Middle East, precisely because supply proved ample (IEA WEO 2025 — BIEE summary).

Gas told a different story.

Global LNG trade set an outright record of 436.98 million tonnes in 2025, a 6.3% jump — the fastest growth since 2022, linking 24 exporting markets with 50 importing markets (Reuters / IGU; TASS / IGU).

Europe’s LNG imports alone surged by 26 Mt to 126.7 Mt as the continent completed its structural pivot away from Russian pipeline gas.

Global liquefaction capacity climbed to 524.5 Mt/y, and the IEA reports final investment decisions for ~300 bcm of new annual LNG export capacity are now scheduled to come online by 2030 — a 50% expansion of world LNG supply, roughly half of it US, another 20% Qatari (IEA WEO 2025 — BIEE; Reuters, 12 Nov 2025).

Even the IEA — historically the most cautious voice on hydrocarbons — revised its natural-gas trajectory upward in the 2025 World Energy Outlook, projecting the LNG market to grow from ~560 bcm in 2024 to 880 bcm by 2035 and 1,020 bcm by 2050 under current-policies scenarios, driven by power-sector demand from AI and data centres (Reuters, IEA WEO 2025).

The message: oil is the marginal barrel of a plateauing system. Gas is the growth vector, and it is being financialised, containerised and geopolitised at a speed no other fuel matches.

2. Six datapoints that share one thread

The country-by-country signals in 2025 all point the same direction — gas is being treated as the dispatchable, exportable, industrially versatile fuel of the transitional decade.

• Pakistan — Mari Petroleum, OGDCL and PPL announced a cluster of onshore discoveries across Sindh, Khyber Pakhtunkhwa and Waziristan through 2025 (Mari Ghazij CFB-1, Faakir-1, Bitrism East-1 at 22.5 MMSCFD + 690 bpd condensate, Spinwam-1, Sehto-1 at 17.2 MMCFD). Mari secured 10 new onshore exploration blocks in the April 2025 DGPC round, and Pakistan’s LNG imports climbed ~10% year-on-year (Arab News; The Nation; Energy Update). Import-substitution and industrial feedstock, not oil, are driving the exploration cycle.

• Cyprus (Aphrodite) — After more than a decade of stasis, the Chevron-led consortium and the Cypriot government agreed an updated development plan in February 2025 and moved the field into FEED by year-end, targeting first gas via a subsea tie-back to Egyptian liquefaction (Reuters, 14 Feb 2025; Offshore Engineer, 23 Dec 2025). Eastern Mediterranean gas is being re-priced as a European energy-security asset.

• Trinidad ↔ Venezuela (Dragon, Manakin-Cocuina) — In an on-again, off-again year, OFAC revoked Trinidad-Venezuela licences in April 2025, then reinstated them in October 2025 for Shell and NGC to develop the Dragon cross-border gas field, with Trinidad now targeting late-2027 first gas into Atlantic LNG’s underutilised trains (Reuters, 8 Apr 2025; Reuters, 9 Oct 2025; Argus, 28 Jan 2026). Gas is treated as a sanctions-adjacent instrument— the licence is the reservoir.

• Norwegian Sea / North Sea — Equinor kept the European supply spine intact with Mistral Sør (Halten, March 2025, 19–44 million boe recoverable), followed by the year’s biggest finds at Lofn and Langemann in the Sleipner area (December 2025, 30–110 million boe), both tie-back candidates to existing gas-export infrastructure feeding continental Europe (Equinor, 5 Mar 2025; Equinor, 5 Dec 2025). Grete Haaland’s line — “Norwegian gas is crucial to Europe’s energy security” — is now industrial policy.

• Indonesia (Andaman / Kutei) — SKK Migas fast-tracked Eni’s Geng North (5 Tcf gas + 400 mmbbls condensate) toward 2027 first gas, then Eni announced a new giant Geliga-1discovery in April 2026 with ~5 Tcf in place, only 20 km north of Geng North (Reuters, Aug 2024; Eni press release, 20 Apr 2026). Combined with Mubadala’s Layaran-1 (6 Tcf) and Tangkulo-1 in the South Andaman block, Indonesia is rebuilding a domestic-feedstock + LNG-export hub (PwC, Oil & Gas in Indonesia 2025).

• Venezuela (Perla / Cardón IV, Manakin) — Despite oil sanctions turbulence, gas licences and joint ventures kept moving: Eni-Repsol Perla continues to feed Venezuelan power, and the BP + NGC Manakin-Cocuina cross-border licence issued in 2024 remained active (Reuters, 19 Feb 2026). Gas is again more politically survivable than oil.

The common thread: in a decade defined by climate policy, sanctions and grid stress, gas has become cleaner than coal, monetizable as LNG, and usable as industrial feedstock and firm power — and every jurisdiction is racing to lock in its share of the 300 bcm expansion wave.

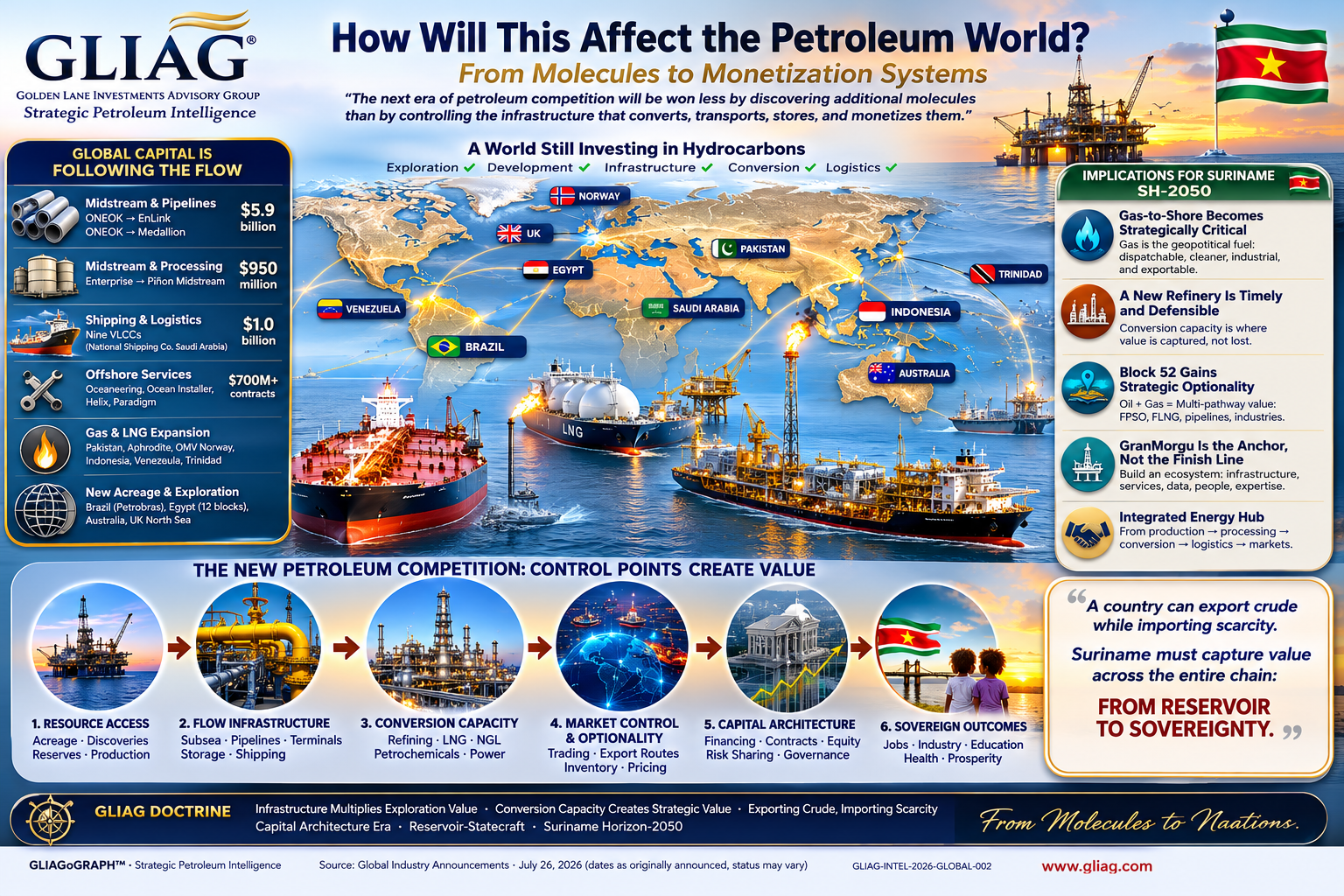

3. Suriname’s position in this reading

This is precisely the terrain the SH-2050 Gas-to-Shore framework was built for. Suriname is not a bystander to the 2025 gas trend — it is a basin participant whose petroleum system is now maturing into a gas-condensate province, not merely an oil play, as I set out in The Emerging Gas-Condensate System of the Guyana–Suriname Basin and Why Gas-to-Shore Infrastructure and New Refinery are Key to Guyana–Suriname Development.

The strategic implications for Suriname line up cleanly with what the global data are showing:

1. Dispatchability wins. The Norwegian and Cypriot experiences confirm that infrastructure adjacency — existing pipelines, LNG terminals, industrial off-takers — is now the deciding development criterion. Suriname’s Golden Lane corridor needs its shore infrastructure planned in parallel with, not after, first gas.

2. LNG-optionality is currency. The Trinidad–Venezuela Dragon story shows that a cross-border gas licence with a liquefaction pathway is worth more than a stranded reservoir. Block 52’s associated gas and any dedicated gas discoveries should be architected from day one for regional monetization — feeding Trinidad-adjacent trains, a Suriname domestic grid, or the self-funding modular refinery as feedstock and firm power.

3. Feedstock, not fuel. Indonesia’s Kutei/Andaman clusters are being developed around ammonia, urea, methanol and power — not just export. This is the case I have been making for a Surinamese downstream chain in Transforming Suriname’s Petroleum into Productive Power and How a Suriname’s New Refinery Can Ensure Energy Security.

4. Fiscal design must match the fuel. Gas is politically stickier than oil, but it also demands longer, thicker contracts (20-year SPAs, HoAs, gas-balancing agreements). This reinforces the fiscal-discipline logic in Navigating Suriname’s Oil Era: A Fiscal Management Guide and Understanding Petroleum Law’s Role in Suriname’s Development.

5. The geopolitical positioning is available now. The window is real but narrow — with ~300 bcm of LNG capacity being sanctioned this decade, the countries that secure off-take, financing and industrial anchor tenants before 2028 will define the 2030s. This is the argument at the heart of Gas as Geopolitical Fuel: Implications for Suriname.

4. Bottom line

2025 was the year the world’s fossil-fuel centre of gravity shifted a notch: oil provided the baseload of the global economy, but gas provided the direction of travel. Pakistan discovered it, Cyprus finally engineered it, Trinidad negotiated it, Norway extended it, Indonesia scaled it, and Venezuela survived on it.

Suriname’s SH-2050 doctrine — Gas-to-Shore infrastructure, a modular downstream refinery, a fit-for-purpose gas law, and a disciplined fiscal envelope — is not a national aspiration written against the global trend. It is written with it. The task in 2026–2028 is execution speed, not strategic reformulation.

Sources — trusted references

• IEA — World Energy Outlook 2025 (BIEE summary) · Gas Market Report Q3 2025 (PDF) · Global Energy Review 2025 (PDF) · Reuters coverage of WEO 2025

• IGU — 2025 World LNG Report · Reuters coverage — 437 Mt record

• OPEC / EIA / Rigzone — OPEC — oil demand >105 mb/d in 2025 · Anadolu Agency, OPEC 2025 share

• Country files — Chevron/Cyprus Aphrodite plan (Reuters) · Aphrodite FEED (Offshore Engineer) · Equinor Mistral Sør · Equinor Lofn / Langemann · Eni Geliga-1 · PwC Oil & Gas in Indonesia 2025 · Trinidad–Venezuela Dragon licence (Reuters) · OGDCL Bitrism East-1 (Arab News) · Mari Ghazij CFB-1 (The Nation) · International oil majors in Venezuela (Reuters)

Companion essays on petroleumenergyinsights.com

• Gas as Geopolitical Fuel: Implications for Suriname

• Why Gas-to-Shore Infrastructure and New Refinery are Key to Guyana–Suriname Development

• The Emerging Gas-Condensate System of the Guyana–Suriname Basin

• Transforming Suriname’s Petroleum into Productive Power

• Suriname Horizon 2050 and Beyond: From Vision to Execution

• Invest in Suriname: A Self-Funding Modular Refinery

• How a Suriname’s New Refinery Can Ensure Energy Security

• Navigating Suriname’s Oil Era: A Fiscal Management Guide

• The Golden Lane Corridor: Suriname’s Oil Future Unfolds

• Repricing the Guyana–Suriname Basin: What’s Driving New Proposals?