From Deepwater Discovery to National & Regional Energy Architecture

1. Introduction: A Structural Sovereign Choice

The Sloanea gas discovery in Block 52 represents a pivotal moment in Suriname’s offshore evolution.

Conceptual modelling based on proxy analogues indicates a recoverable resource range in the order of 1–2 TCF.

At plateau, this corresponds to approximately:

- 150–250 MMcfd gross production (scenario-based)

- 30–50 MMcfd potential Staatsolie 20% entitlement

- 250–400 MW combined-cycle generation potential

The monetisation decision now extends beyond export economics.

It is fundamentally about whether gas remains an offshore commodity or becomes the backbone of national energy transformation.

2. Geological & Production Foundations

Sloanea is interpreted as a deepwater turbidite gas system within the Guyana–Suriname Basin.

Proxy comparison with Mensa (Gulf of Mexico) and Laggan–Tormore (West of Shetland) supports a production-depletion architecture characterized by:

- High initial plateau potential

- Pressure-supported early production

- Gradual exponential decline

- 15–20 year productive life under disciplined development

Scenario modelling suggests cumulative recoverable volumes in the 1–2 TCF range, with production front-loaded over the first decade.

3. Fiscal Architecture & PSC Considerations

Under Suriname’s PSC framework — including reported 10-year tax holiday provisions — public sector income derives from:

- Royalty

- Profit gas share

- Staatsolie participation

- Post-holiday income tax

Scenario-based fiscal modelling indicates:

- Annual public sector revenue: US$150–300 million (mid case)

- Cumulative public revenue (life-of-field): US$3–6+ billion

The tax holiday shifts early cash flow dynamics but does not eliminate long-term public capture under disciplined cost control.

4. Monetisation Pathways

Option 1 – FLNG Export Model

- Indicative NPV: ~US$4.2 billion

- IRR: 18–22%

- Strongest financeability

- Limited domestic multiplier

Option 2 – Gas-to-Shore (20% Entitlement)

- Indicative NPV: ~US$2.8 billion

- IRR: 13–16%

- Moderate capital exposure

- High domestic structural multiplier

Option 3 – Regional Gas Integration (Suriname–Guyana)

- Indicative NPV: ~US$3.5 billion

- IRR: 15–18%

- Higher coordination complexity

- Highest long-term regional scale potential

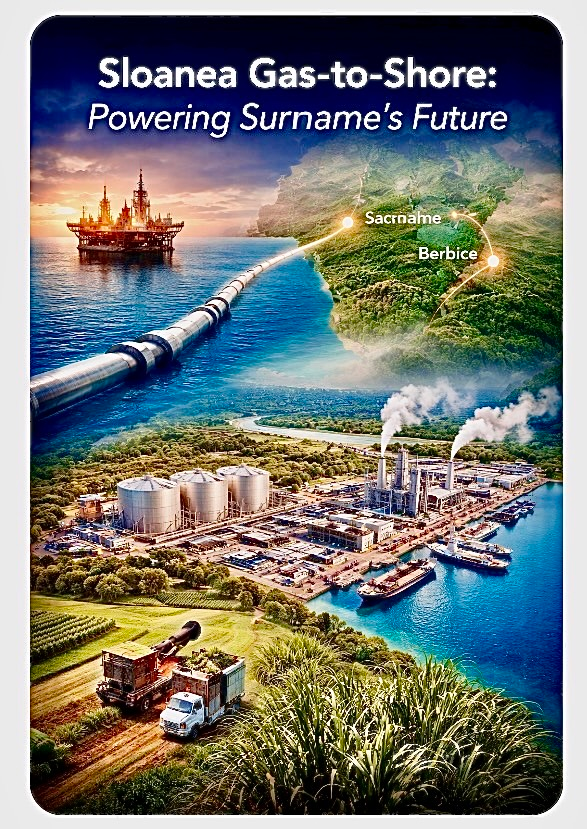

5. Gas-to-Shore: Strategic National Value

Energy Sovereignty

- Major displacement of heavy fuel oil imports

- Reduced Brent-linked tariff volatility

- Improved balance-of-payments stability

- Enhanced sovereign credit profile

Foreign Exchange Stabilisation

Indicative annual oil import substitution potential: US$100–250 million depending on oil price environment.

Over 20 years, cumulative FX savings could reach multi-billion US$ scale.

Electricity System Impact

- 250–400 MW gas-based generation

- 10–20% effective tariff stabilisation potential

- Reduced operational volatility

6. Regional Development — Nickerie as Energy Anchor

Positioning Gas-to-Shore infrastructure in Western Suriname establishes Nickerie as an emerging energy corridor.

Potential spinoffs:

- Industrial estate development

- Agro-processing clusters

- Cold storage logistics

- Port and transport upgrades

- Construction and technical employment multipliers

Construction phase employment: 800–1,500 jobs (indicative range). Permanent operations: 150–300 skilled positions.

7. Regional Integration — Eastern Guyana & Berbice

High-level Suriname–Guyana discussions have highlighted cross-border gas cooperation potential.

A Nickerie–Berbice interconnection could:

- Create supply redundancy

- Increase infrastructure utilisation rates

- Spread fixed costs over larger demand base

- Enhance bilateral economic integration

Energy redundancy lowers sovereign risk and improves financing conditions.

8. Environmental & ESG Alignment

- 20–30% lower CO₂ emissions vs heavy fuel oil

- Reduced sulphur and particulate output

- Improved eligibility for concessional climate financing

Gas-to-Shore strengthens Suriname’s energy transition positioning without compromising energy reliability.

9. Risk & Sensitivity

- -20% production shortfall → IRR compression

- +25% capex overrun → tariff stress

- Utilisation below 65% → infrastructure fragility

- Tariff suppression → fiscal transfer risk

Mitigation mechanisms:

- Firm gas allocation contracts (MDCQ)

- Take-or-pay power purchase agreements

- Blended finance (IFI + commercial)

- Ring-fenced SPV cash flow discipline

10. Recommended Strategic Sequencing

- Secure export monetisation for fiscal stability.

- Contractually secure 20% domestic allocation.

- Deploy right-sized Phase 1 GtS anchored in power generation.

- Evaluate regional integration once supply certainty proven.

This approach balances fiscal prudence with structural transformation.

Conclusion: From Resource to Resilience

Sloanea provides multi-billion public revenue potential. Gas-to-Shore provides structural economic leverage.

Handled conservatively and phased intelligently, Gas-to-Shore becomes:

- An energy sovereignty instrument

- A macroeconomic stabiliser

- A regional development anchor

- A long-term industrial platform

The strategic difference lies not in the gas resource — but in the governance and sequencing of its deployment.

Golden Lane Investments Advisory Group

Strategic Energy Advisory | PSC Design | Fiscal Architecture | Upstream Valuation | Government & IOC Negotiation

Independent advisory at the intersection of subsurface excellence, commercial clarity, and sovereign energy strategy.

© 2026 Golden Lane Investments Advisory Group

Marcel Chin-A-Lien

Global Petroleum & Energy Advisor

Nearly five decades at the highest levels of the energy sector. Giant field discoveries. Multi-billion-dollar deals. The first capitalist upstream ventures in the USSR.

Marcel Chin-A-Lien is one of a rare breed—a technical expert who speaks the language of commerce, negotiation, and geopolitics with equal authority. Four postgraduate degrees across geology, engineering, international business, and management. Fluent in seven languages. Active across Europe, Asia, Africa, and the Americas.

His track record spans giant field discovery, upstream M&A, PSC design, bid round structuring, and fiscal regime optimization—advising national oil companies, IOCs, and supermajors alike. Where others see complexity, he sees opportunity.

Core Expertise: Exploration Strategy · Giant Field Discovery · Upstream M&A & Asset Valuation · PSC Design & Fiscal Optimization · Government & IOC Negotiation · Bid Round Advisory · Technical-Commercial Due Diligence

Credentials: Drs Petroleum Geology · Engineering Geologist · Executive MBA (International Business & M&A) · MSc International Management · Certified Petroleum Geologist #5201 (AAPG) · Chartered European Geologist #92 (EFG) · Energy Negotiator (AIEN) · Cambridge Award – 2000 Outstanding Scientists of the 20th Century · 2× Gold Award, GDF-Suez Paris Innovation Awards (2003)