The Sloanea Gas Development Decision Framework

Hybrid Gas-to-Shore and LNG Export Strategy for Suriname

AUTHOR: Marcel Chin-A-Lien – March 7, 2026.

ROLE: Petroleum & Energy Advisor — Partner, Golden Lane Investments Advisory Group

DOCUMENT TYPE: Policy Brief & Strategic Concept Paper

Disclaimer:

This is my own, private opinion and vision.

I do not represent any government, ministry or any other policy related government institution, anywhere.

Executive Summary

The Sloanea gas discovery in Block 52 gives Suriname a rare opportunity to choose not only how to monetize a resource, but how to shape a national energy system.

This strategic decision is therefore wider than a conventional upstream field-development choice.

It is a question of whether natural gas will be treated mainly as an export commodity or as the anchor resource for a broader Surinamese gas economy.

My report evaluates three commercialization pathways:

Floating LNG (FLNG),

Gas-to-Shore (GtS), and a

Hybrid model combining domestic gas allocation with LNG export of surplus volumes.

The central finding is that the Hybrid model offers the strongest risk-adjusted national value.

Preserving export monetization, improving project financeability, and creating domestic value through lower power costs, avoided fuel imports, and industrial development.

OVERVIEW

Pathway Comparison at a Glance

| OPTION | MAIN STRENGTH | MAIN WEAKNESS | STRATEGIC RANK |

|---|---|---|---|

| Hybrid | Balanced value and financeability | More complex structuring | 1 — Recommended |

| Gas-to-Shore | Maximum domestic development | Higher execution burden | 2 |

| FLNG | Fast export monetization | Limited domestic multiplier | 3 |

SECTION 2

Strategic Context and Policy Alignment

Suriname’s offshore discoveries arrive at a moment when the country needs a credible route to stronger growth, lower electricity costs, and more resilient public finances.

Natural gas is relevant to all three goals. It is cleaner than heavy fuel oil, can support more reliable generation, and can act as both a transition fuel and an industrial feedstock.

In the Surinamese context, this makes gas fundamentally different from crude oil.

The policy logic already articulated in national gas discussions is that oil drives fiscal revenue while gas can create deeper economic structure.

Gas can be brought ashore, converted into power, used as industrial feedstock, and deployed to support downstream capability, giving gas a higher domestic multiplier than oil if infrastructure and regulation are designed properly.

Sloanea should not be judged only by export netback or a narrow upstream NPV.

It should be judged against national objectives: reducing imported fuel dependence, improving electricity affordability, creating industrial optionality, strengthening Staatsolie’s role, and positioning Suriname more strongly in the Guyana-Suriname Basin.

SECTION 3

Development Pathways for Sloanea

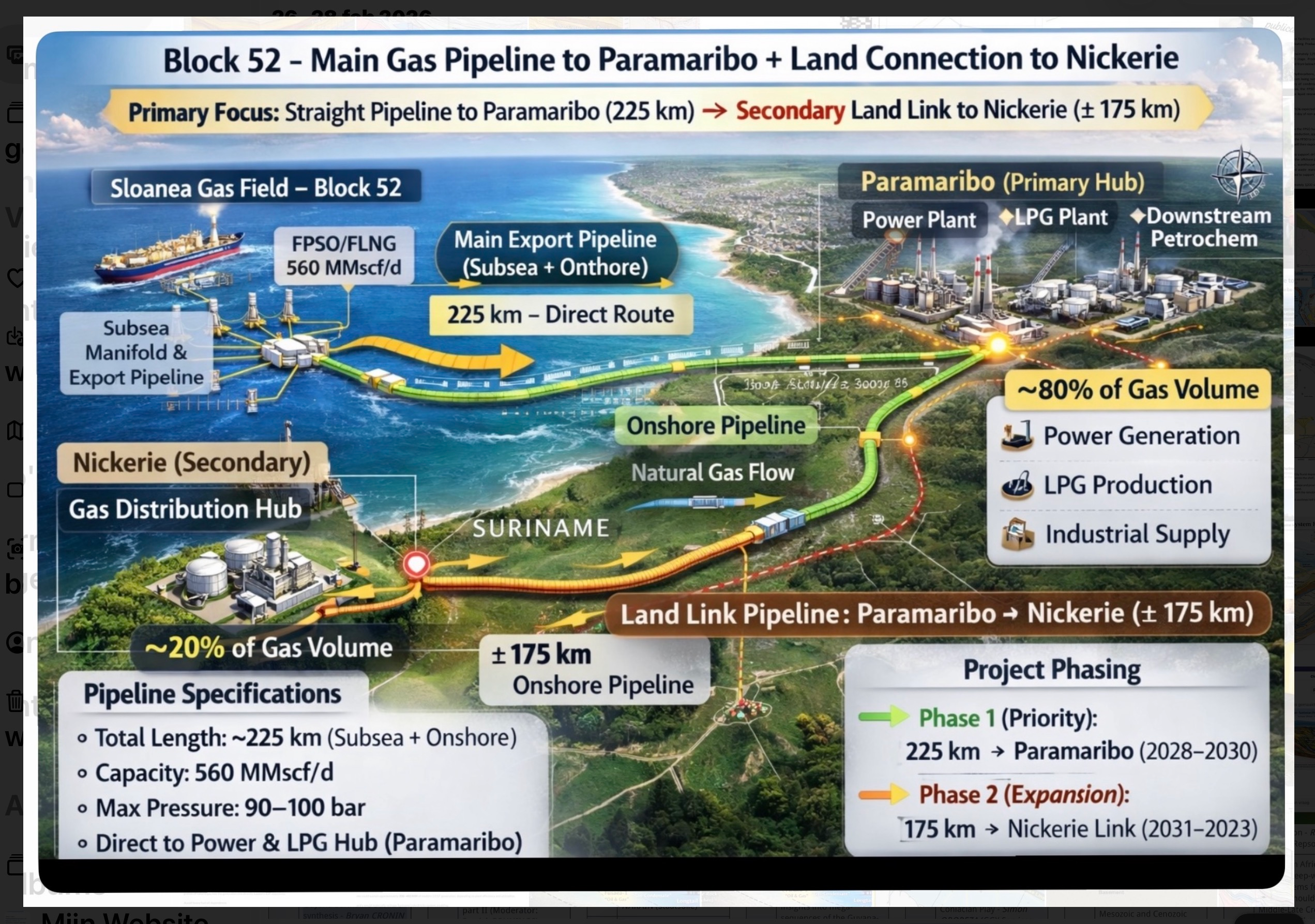

Three commercialization routes are available. Under an FLNG route, gas is liquefied offshore and exported directly to world markets, attractive for speed and simplicity, but leaving most of the value chain offshore with very limited domestic infrastructure.

Under a Gas-to-Shore route, gas is transported by subsea pipeline to an onshore terminal and distributed to power generation and industry.

This route has the strongest domestic development logic, lowering the power-sector fuel bill, enabling gas-based industry, and creating infrastructure that can serve future discoveries.

Its weakness is the need for stronger implementation, contracting discipline, and phased market development.

The Hybrid route combines these two models: part of the gas is reserved for Suriname’s domestic market, especially power and anchor industry, while the balance is exported as LNG.

This structure protects the national-development case without forcing the project to depend entirely on domestic offtake from day one.

Core Proxy Assumptions

| ITEM | BASE-CASE ASSUMPTION |

|---|---|

| Recoverable gas | ~1.5 TCF |

| Plateau production | ~400 MMSCFD |

| Project life | 20 years |

| Indicative start-up window | 2032 |

| Staatsolie participation | 20% |

| Base LNG realized price | USD 9 / MMBtu |

| Base domestic gas transfer value | USD 5.5 / MMBtu |

SECTION 4

Quantifying the Domestic Value of Gas-to-Shore

The most important analytical distinction in this report is between commodity value and system value.

Commodity value is what the gas earns when sold. System value is what the gas enables when used domestically.

For Suriname, system value can be large because imported fuel is expensive, electricity costs remain high, and industrial energy options are limited.

AVOIDED FUEL IMPORTS

$350–450M

Annual range. Improves FX retention and lowers power generation costs.

INDUSTRIAL VALUE-ADDED

$200–500M

Annual range. Supports new sectors, employment, and output growth.

MACRO SPILLOVER

$100–250M

Annual range. Improves national competitiveness across the economy.

Because of these multiplier effects, domestic gas should never be valued only at its transfer price. It should be valued as a development input, the principal reason why a pure export comparison can be misleading for Suriname.

SECTION 5

The National Gas Architecture

A strong Suriname gas strategy needs physical architecture, not just a commercial concept.

The proposed architecture begins offshore at Sloanea, connects via export pipeline to an onshore gas terminal, and branches into three outlets: a Paramaribo energy hub, a Nickerie industrial hub, and an LNG export option for surplus gas.

This architecture creates optionality.

If domestic demand expands faster than expected, more gas can be directed onshore.

If domestic demand develops more slowly, export still provides monetization.

Infrastructure is therefore not only a cost, it is also a strategic hedge.

Once a gas terminal and trunkline exist, other discoveries can be tied back more easily, reducing the economic threshold for future developments.

Infrastructure should be designed with future tie-back and capacity expansion in mind.

The architecture should be viewed as a national platform rather than a single-field evacuation system.

SECTION 6

Economic Value of Staatsolie’s 20% Entitlement

Staatsolie’s participation is not a symbolic item.

It is the key bridge between commercial development and sovereign strategy.

At plateau production of ~400 MMSCFD, a 20% share is roughly 80 MMSCFD — large enough to anchor a meaningful share of domestic power demand and to support early industrial offtake.

| USE OF STAATSOLIE GAS | INDICATIVE VALUE LOGIC | POLICY IMPLICATION |

|---|---|---|

| LNG Export | Strong cash flow but exposed to LNG price cycles | Commercially attractive; limited domestic leverage |

| Power Generation | Avoided HFO/diesel cost plus system savings | High public-value use of gas |

| Anchor Industry | Higher multiplier via jobs and output | Requires staged market development |

In a Hybrid model, Staatsolie’s share becomes particularly powerful.

Securing domestic supply for strategic uses while allowing the rest of the field to participate in LNG export economics.

It allows Suriname to lock in national benefit without undermining the commerciality of the overall project.

SECTION 7

Regional Context: The Guyana-Suriname Basin

Sloanea does not sit in isolation.

It is part of an emerging regional gas province that includes Guyana’s gas developments and wider basin potential.

Please see my other publications on this website, for a grounded view of the gas potential of this basin.

This regional context matters because it changes the strategic value of Suriname’s own infrastructure, if the country waits too long, regional systems elsewhere may set the pace.

The best strategic response is not to rush into weak regional commitments, but to build strength first.

A Surinamese gas system centered on domestic power, anchor industry, and export optionality would improve the country’s regional position and create the possibility of future cross-border collaboration on terms more favorable to Suriname.

SECTION 8

Bank-Grade Economic Comparison

For lenders and policymakers, the correct comparison is risk-adjusted total value, including project value, direct sovereign value, and wider national economic value.

A model that looks strongest on pure export revenue can still be weaker overall if it creates little domestic benefit and no infrastructure legacy.

| CRITERION | FLNG | GAS-TO-SHORE | HYBRID |

|---|---|---|---|

| Speed to first cash | High | Medium | Medium |

| Domestic energy benefit | Low | Very High | High |

| Industrial optionality | Low | Very High | High |

| Infrastructure legacy | Low | Very High | High |

| Risk diversification | Low | Medium | Very High |

| Overall strategic ranking | 3 | 2 | 1 — Strongest |

SECTION 9

Strategic Recommendation

RECOMMENDED PATHWAY

Suriname should pursue a phased Hybrid development strategy for Sloanea, anchored by domestic gas allocation and supported by LNG export optionality.

This is the route most likely to maximize risk-adjusted national value while remaining commercially credible. It monetizes the field while building the country.

The first phase should protect domestic strategic allocation, particularly for power generation and one or two anchor industrial uses.

The second phase should export surplus gas through LNG.

The third phase should expand domestic allocation as market depth, infrastructure, and industrial capability increase.

This recommendation is stronger than a compromise.

It is the route that most closely aligns commercial logic with national policy objectives.

It keeps Suriname open for investment, creates credible export revenues, and uses gas to strengthen the domestic economy.

SECTION 10

Implementation Roadmap, 2030–2045

A successful gas strategy requires sequencing.

The domestic market will not emerge automatically.

It must be built intentionally through policy support, procurement reform, transmission planning, and credible anchor projects.

01

Appraisal & Concept Selection (2026–2028)Gas-quality definition, commercial structure, anchor-demand identification, and pathway decision.

02

FEED, Financing & Contracting (2028–2031)Front-end engineering, project financing, regulatory permitting, and domestic offtake contracting.

03

First Gas & Power Transition (2032–2035)First gas delivery, power-sector transition from HFO/diesel to gas, and initial LNG export.

04

Industrial Scale-Up & Tie-Backs (2035–2045)Expanding industrial demand, new-discovery tie-backs, and broadening the Suriname gas economy.

LNG export capacity should be phased so that it supports — rather than crowds out — domestic value creation throughout this timeline.

SECTION 11

Adaptation Paths: Publication and Ministerial Use

This report can be adapted into two immediate derivative products:

| DERIVATIVE PRODUCT | PRIMARY AUDIENCE | RECOMMENDED EMPHASIS |

|---|---|---|

| Publication Article PetroleumEnergyInsights.com | Energy readers / public policy audience | Narrative, basin context, energy-transition implications, nation-building logic |

| Ministerial Briefing Deck | Cabinet, ministries, Staatsolie leadership | Decision matrix, economic figures, Staatsolie’s role, implementation roadmap |

SECTION 12

Conclusions

Sloanea should be viewed as the first major design test for Suriname’s gas future.

A narrow export lens would understate the field’s real potential.

When gas is assessed as a platform for electricity transition, industrial development, infrastructure creation, and sovereign capability, the strategic picture changes materially.

The strongest overall conclusion of this report is clear:

Suriname should pursue a phased Hybrid development strategy for Sloanea, anchored by domestic gas allocation and supported by LNG export optionality.

This is the route most likely to maximize risk-adjusted national value while still being commercially credible.

If implemented well, this strategy can mark the beginning of the Suriname gas economy, rather than simply the export of another offshore commodity.

Source note: This policy brief was developed using the strategic framework discussed in the translated Presidential Study Group presentation on gas exploitation and the subsequent analytical work developed in this project. But it represents my own, independent vision on this subject.

© 2026 Golden Lane Investments Advisory GroupMarcel Chin-A-Lien · Petroleum & Energy AdvisorPolicy Brief — March 2026