A GLIAG Strategic Insight Note

Golden Lane Investments Advisory Group (GLIAG)

Marcel P.T. Chin-A-Lien – Petroleum & Energy Advisor

June 2026

1. Executive summary

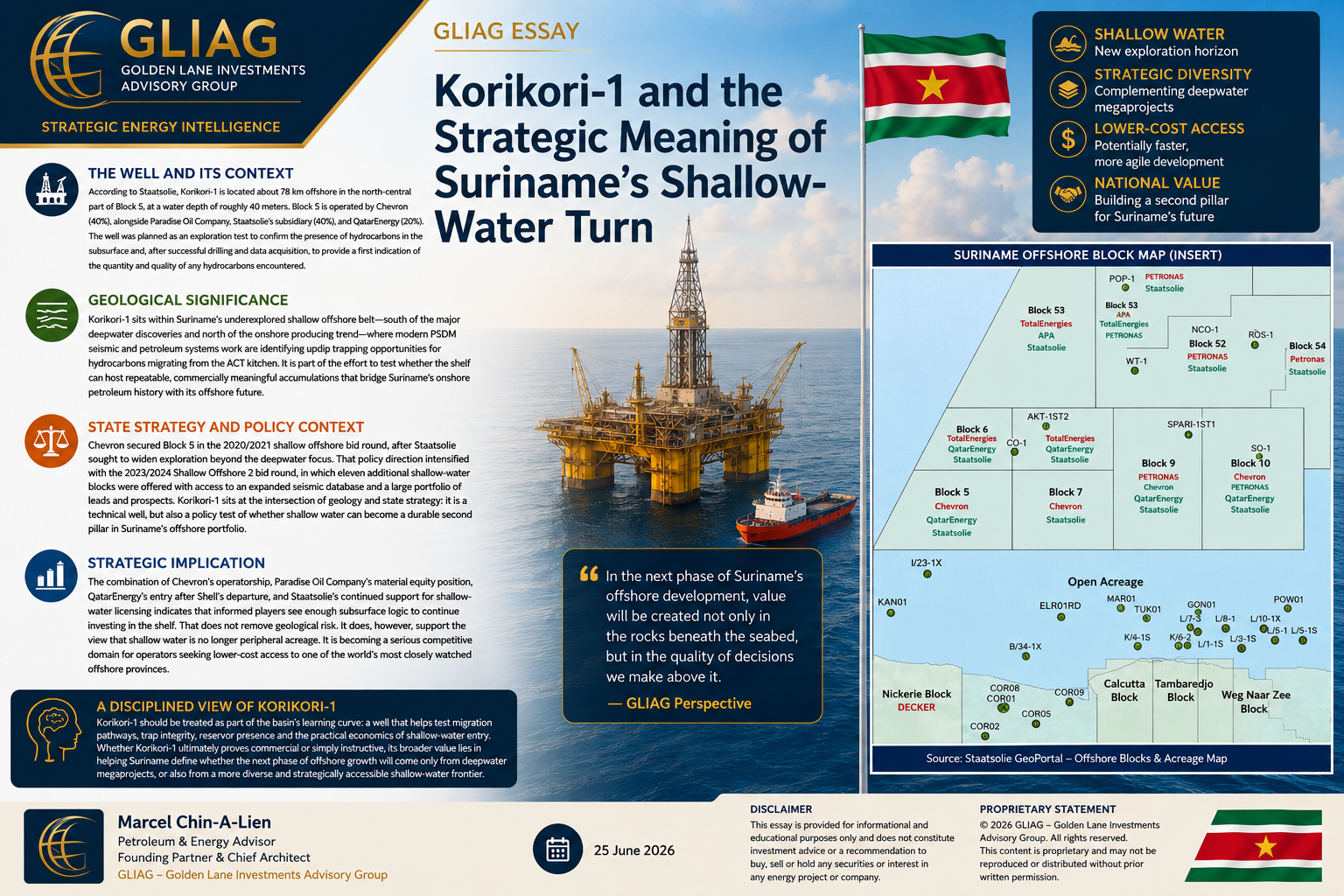

Korikori-1 is Chevron’s flagship shallow-water wildcat in Suriname’s Block 5, drilled in late 2025 in approximately 40 metres of water about 78 kilometres offshore, with Paradise Oil Company and QatarEnergy as partners.

As of mid-2026, no official discovery announcement or flow-test data have been released, but the well already shifts perceptions: Suriname’s offshore is no longer a deepwater-only story; it is evolving into a layered basin in which shallow water becomes a serious, lower-cost entry point into the Guyana–Suriname system.

For Suriname, Korikori-1 is less a verdict than a learning event.

It sits inside a deliberate state strategy to open eleven shallow-offshore blocks, underpinned by modern 3D seismic, petroleum-systems modelling and a portfolio of more than ninety mapped leads with aggregate unrisked in-place volumes estimated around ninety billion barrels.

The central question is no longer whether the deepwater kitchen works, but whether the shelf can deliver repeatable, commercially robust accumulations under a competitive yet disciplined fiscal regime.

For operators and investors, Korikori-1 reframes risk rather than removing it.

Deepwater FPSO projects anchored by multi-billion-barrel discoveries remain the backbone of value creation, but shallow-water prospects now offer shorter cycle times, lower unit well costs and a more accessible entry route – with higher play risk and greater dependence on host-country execution.

Key messages

• Korikori-1 is a signal, not yet a verdict: a drilled wildcat with undisclosed results that confirms major-company commitment to Suriname’s shelf.

• Shallow water now forms a distinct risk–reward tier alongside deepwater, combining lower capital intensity with earlier-stage geological uncertainty.

• For Staatsolie, shallow-water rounds are a tool to widen participation and strengthen bargaining power; for bidders, they are option value, not a licence for overbidding.

• GLIAG’s view: fold Korikori-1 into a portfolio-based Suriname strategy, rather than using it as a single-well proxy for the basin.

2. Context and objectives

Over the past decade, the Guyana–Suriname Basin has moved from frontier to global reference point for deepwater value creation, anchored by multi-billion-barrel discoveries in Guyana’s Stabroek Block and Suriname’s Block 58. On the back of this success, Suriname has launched successive shallow-offshore bid rounds and awarded key blocks, including Block 5, to supermajors and national partners to test whether the shelf can join this value arc.

This note has three objectives.

First, to summarise what is publicly known – and deliberately not yet known – about Korikori-1.

Second, to situate the well in its geological and institutional context within the shallow-offshore corridor.

Third, to assess implications for future shallow-water bidding, portfolio design and Suriname’s long-term transition agenda, including GLIAG’s Suriname Horizon 2050 and gas-to-shore concepts.

3. Shallow-water play fundamentals

Block 5 lies in Suriname’s western shallow offshore, roughly 45–82 kilometres from shore in water depths of 30–60 metres, between the mature onshore belt and the deepwater discovery trend.

This position gives Korikori-1 a distinctive role: it tests whether hydrocarbons generated in the deep kitchen and trapped in deepwater turbidite complexes can also charge viable traps on the shelf.

Multi-client 3D campaigns and Staatsolie-led petroleum-systems studies have mapped a dense inventory of structural and stratigraphic leads across the shallow offshore.

Aptian and ACT source rocks are interpreted as mature beneath much of the shelf, with migration pathways toward updip traps that range from tilted fault blocks to subtle stratigraphic pinch-outs.

Korikori-1 is one of the first wells to turn this geophysical picture into hard geological evidence, closing the loop between GeoAtlas-level basin interpretation and actual shelf drilling.

Staatsolie’s GeoAtlas and supporting petroleum-geology pages provide the most authoritative public synthesis of this context.

They place Suriname’s segment of the Guiana Basin within the broader passive-margin framework, summarise stratigraphy, structural elements and proven petroleum-system components, and link them to both deepwater and shallow-water prospectivity. For any serious analysis of Korikori-1’s geological meaning,

the GeoAtlas and associated GeoPortal are baseline references rather than optional extras.

4. Korikori-1 – facts and signals

Public disclosures deliberately keep Korikori-1 factual and concise.

Staatsolie’s October 2025 notice confirms that Chevron operates Block 5 with a 40% interest, alongside Paradise Oil Company with 40% and QatarEnergy with 20%; that the National Environmental Authority granted the drilling permit in mid-2025; that the Noble Regina Allen jack-up is contracted; and that drilling operations were expected to last around ninety days.

Dutch-language communications reinforce the same equity split and operational framing for Surinamese stakeholders.

Independent technical commentary, including GLIAG-linked analysis, lists the well as “drilled – awaiting formal disclosure; no transformational discovery reported”.

This phrasing is important. It constrains speculation, confirms that the well is part of the basin’s learning record and underlines that Korikori-1 should be treated as a calibration datapoint rather than as a declared value anchor. Social-media updates and trade press reports on rig mobilisation add colour on timing and operations but provide no additional subsurface information.

From a GLIAG perspective, the discipline is to hold that line: recognise Korikori-1 as a significant investment in a still-emerging shallow-water play, while resisting the temptation to infer flow-rates or reserves where the operator and state have chosen not to disclose them.

5. Nearshore Staatsolie wells: calibration before Korikori-1

Long before Korikori-1 tested Suriname’s shallow-offshore shelf in Block 5, Staatsolie had already run two nearshore drilling campaigns that framed today’s risk perception.

In 2015 the company launched a six-month programme in nearshore Block 4, initially envisaging nine exploration wells and marking the first time Staatsolie carried out a fully self-operated offshore exploration campaign.

Market conditions forced a reduction to five wells, but the 2015 annual report notes that four showed promising indications of hydrocarbons, with oil encountered in the first two wells and final petrophysical and test results scheduled for early 2016.

These were modest wells in shallow water, but they confirmed that an active petroleum system extended into Suriname’s nearshore and that Staatsolie could manage offshore drilling risk on its own balance sheet.

The 2019 Nearshore Drilling Project took that learning several steps further.

Under project manager Tom Ketele, Staatsolie prepared a nine-well campaign (some public material refers to ten prospects) in water depths of roughly 8–25 metres, designed to safeguard long-term production by detecting nearshore reserves.

In execution, six exploration wells were drilled from the jack-up West Castor – Marai, Electric Ray, Kankantrie, Powisi, Gonini and Tukunari – to total depths between about 1,000 and 3,000 metres, with the remaining locations dropped as operational experience and evolving subsurface insight made them lower priorities.

No commercial oil discovery was made, but four of the six wells recorded oil shows, and Staatsolie emphasised that the project delivered very valuable data, sharpened geological insight and increased future chances of success, within planned time and budget and without environmental incidents.

For today’s shallow-water portfolio this history matters.

The 2015 Block 4 wells and the 2019 Nearshore Drilling Project did not generate headline reserves, but they created an operational and geological foundation: they proved that the coastal petroleum system is active, demonstrated Staatsolie’s ability to manage multi-well nearshore campaigns, and generated datasets that now feed into the GeoAtlas, data catalogues and shallow-offshore bid material.

In that sense, Korikori-1 does not stand alone.

It is the first major-company wildcat in a shallow-water corridor that Staatsolie has already de-risked through its own nearshore drilling – moving the conversation from whether there is oil in the coastal belt to whether the shelf can deliver repeatable, commercial accumulations at scale.

6. Implications for shallow-water bidding

Shallow-water Suriname now offers a distinct risk–reward tier. Unit well costs and logistics are materially lower than in deep water, and potential tie-backs to future infrastructure can shorten time to cash flow; however, the play is earlier in its calibration, and commercial volumes at scale have yet to be demonstrated. Rational bidders will therefore emphasise robust seismic and multi-well work programmes, maintain conservative geological risking and avoid deepwater-style signature bonuses.

For Staatsolie, Korikori-1 validates the decision to put shallow water at the centre of policy rather than leaving it as residual acreage. The 2023/24 Shallow Offshore 2 bid round, comprising eleven blocks with modern seismic coverage, a prospect inventory of more than ninety leads and aggregate mean unrisked STOIIP of around 91 billion barrels, allows the state to benchmark operator quality, work commitments and local-content proposals more effectively than a single deepwater beauty contest. Subsequent open-door offerings further extend this logic, with Staatsolie explicitly directing potential entrants to the GeoAtlas and GeoPortal to build a shared geological starting point.

For companies unable to access the deepwater core, shallow-offshore blocks become a credible alternative: a way to gain exposure to the Guiana Basin’s petroleum system with lower capital intensity but higher play risk. For those already embedded in the basin, shallow water offers portfolio diversification, potential gas and liquids close to shore, and a platform for local-content and infrastructure strategies that are more visible to the Surinamese public.

7. GLIAG view and next steps

GLIAG’s central view is that Korikori-1 should be understood as part of Suriname’s institutional learning curve, not as a binary success or failure. Even without public test data, the well already shifts perceptions of the shelf, informs fiscal design and helps define how far Suriname can move from resource discovery towards capability building and state resilience.

Next steps for serious stakeholders are clear. Treat shallow water as a structured exploration programme rather than a one-well bet, sequencing wells, seismic and studies across the shelf. Integrate shallow-water entries into Suriname’s broader Horizon-2050 transition architecture, including gas-to-shore, downstream industrialisation and institutional strengthening. Anchor investment decisions in disciplined risk analysis and transparent references – Staatsolie’s GeoAtlas, GeoPortal and bid documentation – rather than in narratives alone.

For additional context on Block 5 and the narrative surrounding the “Red Ibis” wildcat, see the companion essay “Korikori-1 wildcat: De Rode Ibis van Chevron en Staatsolie in Q4 2025” on Petroleum Energy Insights.

8. Annex – References and data gateways

• Staatsolie Maatschappij Suriname N.V. (2025). ‘Drilling of Korikori-1 Exploration Well to Begin in Block 5.’ Official announcement detailing location, partners, water depth, rig and drilling objectives. https://www.staatsolie.com/en/news/drilling-of-korikori-1-exploration-well-to-begin-in-block-5/

• Staatsolie Maatschappij Suriname N.V. (2025). ‘Start booractiviteiten exploratieput Korikori-1 in blok 5.’ Dutch notice confirming Chevron, Paradise Oil Company and QatarEnergy equity and Noble Regina Allen deployment. https://www.staatsolie.com/nl/nieuws/start-booractiviteiten-exploratieput-korikori-1-in-blok-5/

• Oil & Gas Journal (2023). ‘Suriname begins offshore bid round.’ Overview of the Shallow Offshore 2 bid round and shallow-offshore prospectivity. https://www.ogj.com/general-interest/article/14301261/suriname-begins-offshore-bid-round

• Staatsolie Maatschappij Suriname N.V. (2023). ‘Suriname Shallow Offshore 2 Bid Round 2023–2024 Announced.’ Official description of SHO2, eleven blocks and bid timetable. https://www.staatsolie.com/en/news/suriname-shallow-offshore-2-bid-round-2023-2024-announced/

• Local Content Suriname (2024). ‘Staatsolie Invites Bids for Shallow Offshore Blocks in Suriname.’ Context on basin location and Staatsolie’s ambition to become ‘Master of the basin.’ https://localcontentsuriname.com/nieuwsbericht/staatsolie-initiates-bidding-round-for-eleven-blocks-in-shallow-offshore-area/

• TGS Multi-Client. ‘Suriname Shallow Water Bid Round | Seismic Data.’ Seismic coverage and play description for the shallow-offshore blocks. https://www.tgs.com/seismic/multi-client/latin-america/suriname/shallow-water-round

• Petroleum & Energy Insights / GLIAG (2026). ‘Offshore Suriname Exploration 2025–2026: Facts, Expectations and Basin Reality.’ Technical review listing Korikori-1 as ‘drilled – awaiting formal disclosure; no transformational discovery reported.’ https://petroleumenergyinsights.com/offshore-suriname-exploration-2025-2026-facts-expectations-and-basin-reality/

• Staatsolie – GeoAtlas of Suriname. Integrated summary of Suriname’s petroleum geology within the Guiana Basin; core reference for basin-scale analysis. https://www.staatsolie.com/en/shi/geoatlas/

• Staatsolie GeoPortal. Interactive GIS platform providing access to seismic, wells and licensing data. https://geoportal-staatsolie.hub.arcgis.com

• Staatsolie – ‘Open-Door Offering.’ Framework for accessing remaining offshore acreage; explicitly references GeoAtlas and GeoPortal as primary geology and data gateways. https://www.staatsolie.com/en/open-door-offering/