GLIAG · Golden Lane Investments Advisory Group – NEW MODULAR REFINERY SURINAME

GLIAG

GOLDEN LANE INVESTMENTS ADVISORY GROUP

INVESTOR POSITIONING ESSAY · NEW MODULAR REFINERY SURINAME

The Refinery as Sovereign Instrument

How the BPM6 current-account swing turns a downstream project into a midsize eurobond, every year, without debt

SUBJECT The BPM6 current-account swing and its rating relevance for the New Modular Refinery Suriname

SERIES GLIAG Advisory Intelligence · Ref. GLIAG-TECH-2026-BPM6-001 –

Intellectual Property, Copyright and Licensing Notice

© 2026 GLIAG N.V. – Golden Lane Investments Advisory Group. All rights reserved.

This publication, including its text, analyses, concepts, methodologies, diagrams, GLIAGoGRAPHs™, figures, tables, and visual designs, constitutes the intellectual property of GLIAG N.V. and/or its authors. No part may be reproduced, distributed, modified, or used for commercial purposes without prior written permission, except where permitted by applicable copyright law.

DATE 14th July 2026

Written by Marcel Chin-A-Lien – Petroleum & Energy Advisor – Principal Founding Partner & Chief Architect of GLIAG N.V. – Golden Lane Investments Advisory Group – Paramaribo, Suriname 7 The Netherlands

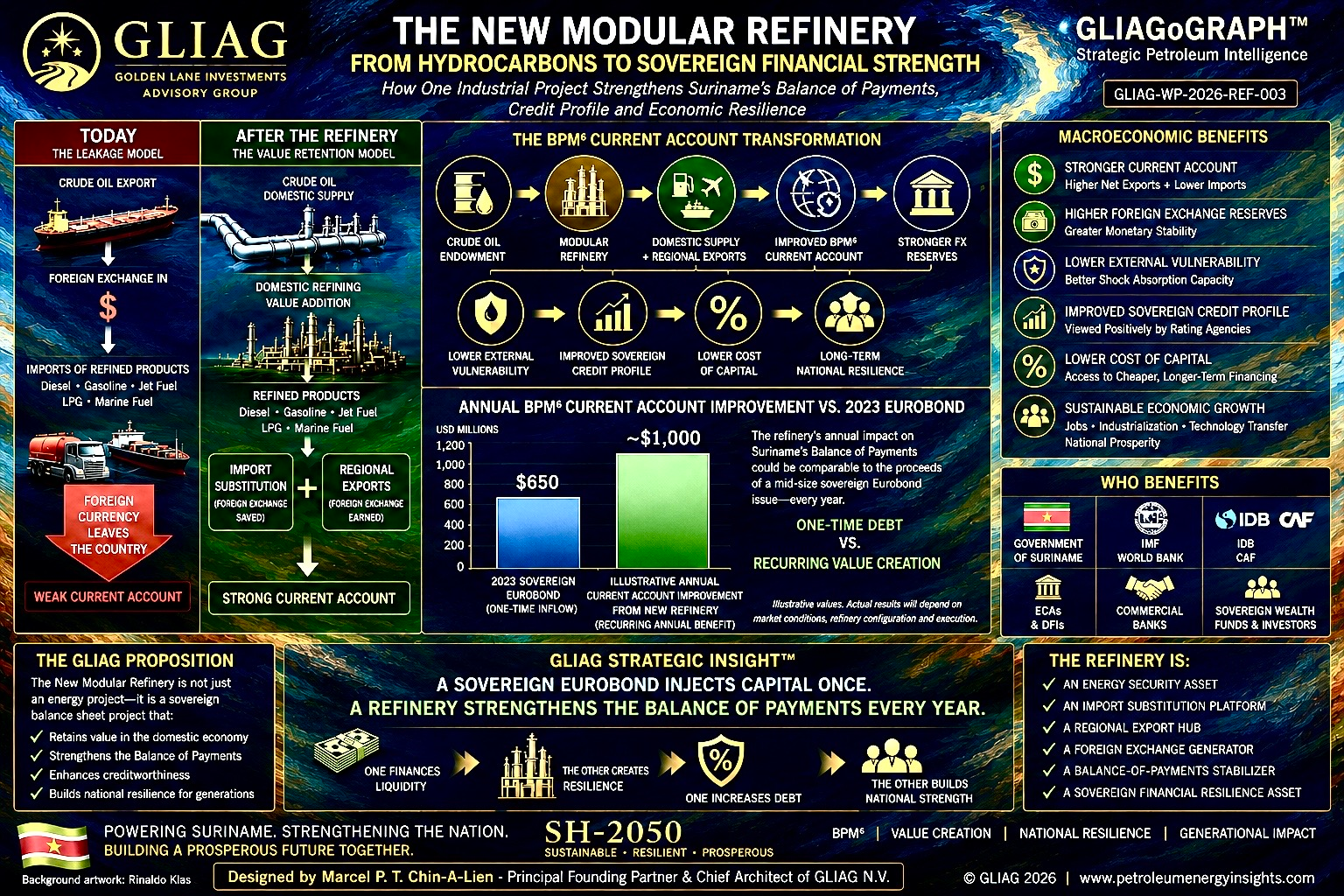

A Downstream Project Measured in Sovereign Units

The core claim is simple to state and consequential to prove: the New Modular Refinery shifts Suriname’s current account by an amount macroeconomically comparable to a midsize sovereign eurobond — every year, structurally, without adding a dollar of external debt.

GLIAG’s investment thesis for the New Modular Refinery has, until now, been argued primarily in project-finance terms: capacity, feedstock, offtake, capital expenditure, and bankability envelope. This essay makes a different case — a macro case. It asks what the refinery does not to a project balance sheet but to the Republic of Suriname’s external position, as measured the way the IMF, the rating agencies, and the eurobond market actually measure it: under BPM6.

What follows unpacks that claim in five movements: what BPM6 is and why the framework matters; what the current-account swing consists of; how large it is in hard USD terms; how it compares to Suriname’s 2023 restructured eurobond; and why rating agencies will treat it as sovereign-relevant rather than merely commercial.

The Measurement Standard: BPM6

BPM6 is the sixth edition of the IMF Balance of Payments and International Investment Position Manual — the global standard by which central banks, including the Central Bank of Suriname (CBVS), report their balance of payments. Suriname reports under BPM6 with IMF technical assistance, documented in IMF Country Report 22/118 (August 2020).

Within BPM6, the current account is built from four blocks, and the refinery’s effect lands squarely in the first:

— Goods — exports minus imports (where the refinery swing lands)

— Services

— Primary income — interest, dividends, wages

— Secondary income — transfers, remittances

When GLIAG refers to the ‘BPM6 current-account swing,’ the reference is literal: the same line item that the IMF, S&P, Moody’s, Fitch, and institutional bondholders examine to judge whether a country structurally earns or loses foreign exchange. This is not a proprietary GLIAG metric — it is the metric the market already uses to price Suriname’s risk.

Anatomy of the Swing

Import substitution

Suriname currently imports refined products — diesel, gasoline, jet fuel, LPG, and heavy fuel oil. Once the refinery is operational, a large share of that import line disappears from the debit side of the goods balance. The current account improves directly, mechanically, without requiring a single new export contract.

Regional export tail

Capacity above domestic demand does not sit idle — it is exported to the region: the Caribbean, Guyana, French Guiana, and potentially northern Brazil. This generates additional credits on the goods balance, layered on top of the import-substitution effect.

Both effects push in the same direction. The goods balance — and therefore the current account — improves structurally, year after year, for the operating life of the plant.

Quantifying the Swing

Assumptions

— Modular capacity: 15,000 bpd effective net capacity

— Domestic demand: approximately 8,000 bpd, including growth from the oil industry and downstream activity

— Net export surplus: approximately 7,000 bpd × 350 operating days

— Product price: USD 85–110/bbl, crack-adjusted diesel/gasoline/jet mix

— Import baseline: USD 225 million (UN COMTRADE 2024), rising to USD 500 million in the high case as domestic demand grows

The annual structural swing

| Component | Low case | Base case | High case |

| Import substitution of refined products | USD 225 mln | USD 350 mln | USD 500 mln |

| Regional export tail | USD 208 mln | USD 233 mln | USD 270 mln |

| Total BPM6 CA-swing | USD 433 mln | USD 583 mln | USD 770 mln |

| As % of 2025 GDP (USD 4.52 bn) | +9.6% GDP | +12.9% GDP | +17.0% GDP |

Table 1 — Annual BPM6 current-account swing by scenario, in USD million and as % of 2025 GDP.

The GDP percentages are the decisive metric. Rating agencies assess current-account positions consistently as a share of GDP, not in absolute dollars. A structural improvement of +9.6% to +17.0% of GDP is sovereign-relevant by definition — it is not a marginal line item that disappears into rounding on a national accounts table. It is large enough, on its own, to move the number the market watches most.

Calibration Against the 2023 Eurobond

For calibration: Suriname’s restructured 2023 eurobond amounted to USD 660 million, with estimated flow relief of USD 900 million over 2023–2026 (Reuters; Government of Suriname). A ‘midsize sovereign eurobond’ for a frontier market typically ranges between USD 500 million and USD 1.5 billion — placing the refinery’s annual swing squarely inside that reference class, on a recurring basis.

Chart 1 — Annual CA-swing versus the 2023 eurobond principal (left), and 10-year cumulative impact under the base case, nominal and NPV @ 8% (right).

| Instrument | Size | Character | Debt build-up |

| 2023 restructured eurobond | USD 660 mln | One-off, principal | Yes — 7.95%–10.5% coupon |

| Flow relief 2023–2026 | USD 900 mln | 4-year relief | Yes — restructuring |

| Refinery CA-swing (base case) | USD 583 mln / year | Structural, recurring | No — zero |

| NPV 10 years @ 8% discount | USD 3,910 mln | ≈ 5.9× eurobond | — |

Table 2 — The 2023 eurobond compared with the refinery’s base-case current-account swing.

The annual base-case swing equals 88% of the size of the 2023 eurobond principal — but recurring. In NPV terms over ten years at an 8% discount rate, the swing equates to roughly 5.9× the eurobond.

Put differently: the macro impact on Suriname’s external position is nearly a full midsize sovereign issue every single year — without debt build-up and without FX-denominated interest cost. The eurobond bought Suriname breathing room through 2026. The refinery, once operational, manufactures that same breathing room domestically, indefinitely.

Why This Is Rating-Relevant

Suriname is currently rated Caa1 by Moody’s (positive outlook, following the two-notch upgrade of October 2024) and CCC+ by S&P — deep in speculative grade, with the rating partly reflecting external vulnerability. The IMF’s 2025 Article IV concluding statement (20 November 2025) explicitly frames the external position as the critical recovery path.

Rating agencies weigh three external factors most heavily, and the refinery swing works favourably on all three — precisely when the 2025–2027 oil-FDI cycle pushes the current account temporarily deep into deficit through import-heavy Block 58 development.

| Rating driver | Current position (IMF 2025) | Refinery impact (base case) |

| Current account / GDP | 2025: −35.3% | 2026: −51.4% (Block 58 FDI imports) | Offsets ~35–40% of deficit; structural buffer post-2028 |

| FX reserves (months of imports) | 2026: USD 1,279 mln = 2.8 months cover | +2 to +3 months cover within 2–3 years of operation |

| External debt build-up | Debt/GDP ~86% (2025) | Reduces refinancing need — no new FX debt required |

Table 3 — IMF-reported rating drivers versus the refinery’s structural impact.

A refinery that structurally improves the goods balance by sovereign-scale amounts delivers three effects simultaneously on the rating:

— Narrows the current-account deficit (or turns it to surplus post-Block 58) → lower external financing need

— Builds FX reserves at CBVS → stronger debt-service coverage

— Reduces dependence on external capital markets → lower refinancing risk

The Investor Case, Stated Plainly

New Modular Refinery Suriname — a BPM6 current-account swing of sovereign scale, comparable to a midsize eurobond, structural and without debt. The modular refinery shifts approximately USD 430–770 million per year on Suriname’s BPM6 current account. That is 65% to 117% of the 2023 eurobond principal — annually, structurally, and without external debt build-up. The effect is directly visible in CBVS reserve coverage and materially moves Suriname’s sovereign rating trajectory.

| Metric | Base case | Reference |

| Annual CA-swing | USD 583 mln | 2023 eurobond: USD 660 mln (one-off) |

| Impact as % GDP | +12.9% GDP | 2025 GDP: USD 4.52 bn |

| NPV 10 years @ 8% | USD 3,910 mln | ≈ 5.9× the 2023 eurobond |

| Debt build-up | Zero | Eurobond: 7.95–10.5% coupon |

| FX reserve increase | +2 to +3 months cover | Current: 2.8 months (fragile) |

Table 4 — Key figures for direct inclusion in the GLIAG investor deck.

This refinery is not a sector project — it is a macro instrument. Every operational day shifts dollar flows visible in CBVS BPM6 reporting. For rating agencies, the IMF, and the secondary eurobond market, that is a weightier signal than an equivalent sovereign issuance, because it generates no debt and is recurring. For equity investors, it means the project’s macro risk profile justifies a lower country risk premium than a comparable downstream investment in a lower-rated frontier market.

GLIAG position

The project should be positioned in the investor deck along two tracks — project finance and sovereign macro narrative. The two tracks reinforce each other in the bankability case: the first shows the plant can be built and financed; the second shows why the state, the IMF, and the rating agencies have an independent interest in seeing it built.

Sources

IMF & Multilateral

— IMF Balance of Payments and International Investment Position Manual (BPM6) — imf.org

— IMF Suriname: 2024 Article IV Consultation and Eighth Review, December 2024 — imf.org

— IMF Staff Concluding Statement, 2025 Article IV Mission, 20 November 2025 — imf.org

— IMF Suriname Technical Assistance Report, External Sector Statistics, Country Report 22/118 — elibrary.imf.org

Central Bank & Government of Suriname

— CBVS Balance of Payments — cbvs.sr

— Government of Suriname — Restructuring of bondholders finalized, December 2023 — gov.sr

— Suriname Debt Management Office — Q1 2024 Report — sdmo.org

Rating Agencies & Market

— S&P Global Ratings — Republic of Suriname Foreign and Local Currency Ratings — spglobal.com

— Moody’s Ratings affirms Suriname’s ratings at Caa1 — surinamenieuwscentrale.com

— Reuters — Suriname reaches debt restructuring deal with bondholders, May 2023 — reuters.com

— LatinFinance — Sovereign Restructuring of the Year 2024 (Suriname) — latinfinance.com

Trade Data & Macro

— UN COMTRADE via Trading Economics — Suriname Imports Mineral Fuels 2024 — tradingeconomics.com

— World Bank — Suriname GDP data — data.worldbank.org

— OEC — Refined Petroleum trade profile, Suriname — oec.world

Disclaimer: this document contains indicative macro calculations based on public sources and model assumptions for capacity, prices, and operational availability. Actual figures depend on final project parameters (FEED, offtake contracts, financing structure) and market conditions. This note does not constitute investment advice or an offer.

© 2026 GLIAG — Golden Lane Investments Advisory Group. Where Information Becomes Intelligence. Where Discoveries Become Strategy.

CONFIDENTIAL · GLIAG-TECH-2026-BPM6-001Page of