The Infrastructure Turn

What a single season of global petroleum deals reveals about the next decade — and why Suriname should be listening

Drs. M.P.T. Chin-A-Lien, MBA, M.Sc., Ing. Geologist – 11 July 2026

Certified Professional Geologist Nr. 5201-1996 (AAPG) · Chartered European Geologist Nr. 92-1996 (EFG) · Energy Negotiator, June 2021 (AIEN)

Principal Founding Partner & Chief Architect, GLIAG

GLIAG-INTEL-2026-GLOBAL-001 · Paramaribo / Delft

A basin’s future is no longer decided only by what is found beneath it. Increasingly, it is decided by what is built around it.

Most petroleum news arrives as noise: a transaction here, a discovery there, a licensing round somewhere else. Read individually, each item is a data point. Read together, across a single season, they become something else — a signal.

GLIAG does not treat industry news as reportage. We treat it as evidence. And the evidence from this season’s global deal flow points to a shift with direct consequences for Suriname’s national strategy.

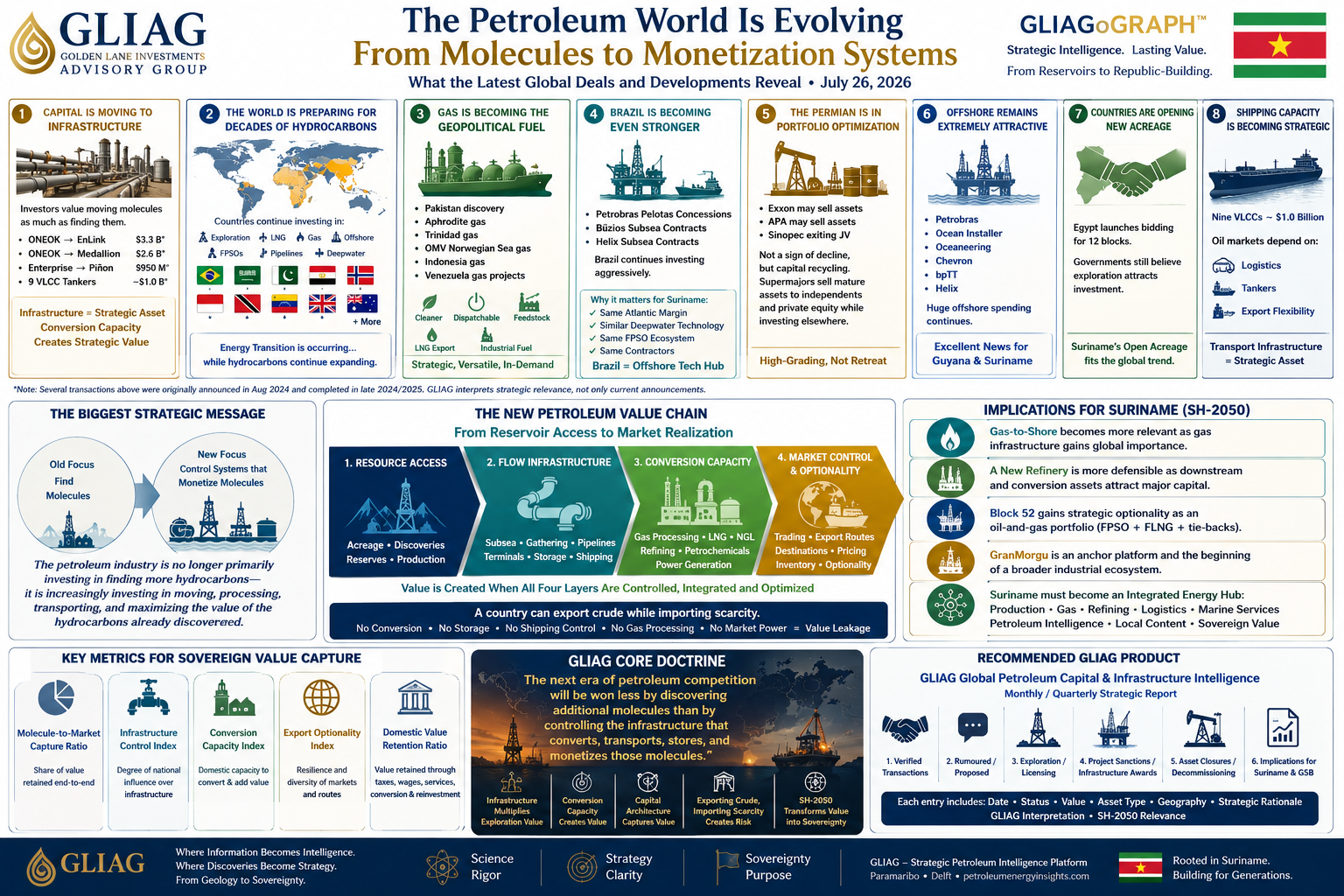

Capital is no longer chasing molecules. It is chasing the systems that move, convert, and monetize them.

01 – Capital Is Migrating Downstream of Discovery

Across recent transactions, the largest sums are not attached to exploration. They are attached to midstream, pipelines, storage, LNG, shipping, and processing — the connective tissue of the industry rather than its source rock.

| TRANSACTION TYPE | SIGNAL |

|---|---|

| Midstream consolidation (ONEOK–EnLink, ONEOK–Medallion) | Multi-billion dollar bets on gathering and takeaway capacity |

| Gas processing (Enterprise–Piñon Midstream) | Value migrating toward treatment and conditioning assets |

| Tanker fleet acquisition (nine VLCCs, ~USD 1 billion) | Logistics itself becoming a strategic holding |

The pattern is unambiguous: investors increasingly believe that moving hydrocarbons is becoming as valuable as finding them. This is precisely the logic behind GLIAG’s long-standing position that Conversion Capacity creates strategic value in its own right — independent of, and additive to, reserve size.

02 – The World Is Not Behaving Like Hydrocarbons Are Ending

Brazil, Saudi Arabia, Pakistan, Egypt, Norway, Indonesia, Trinidad, Venezuela, the United Kingdom, and Australia are, simultaneously, investing in exploration, LNG, gas monetization, offshore development, and pipeline capacity. Governments across radically different political systems and income levels are making the same wager.

The energy transition is real. It is also, evidently, not a reason for capital or governments to abandon hydrocarbon infrastructure. The two processes are occurring on the same timeline, not in sequence.

03 – Gas Is Becoming the Geopolitical Fuel

Discoveries and developments in Pakistan, Cyprus (Aphrodite), Trinidad, the Norwegian Sea, Indonesia, and Venezuela share a common thread: gas is being treated as the dispatchable, exportable, industrially versatile fuel of this transitional decade — cleaner than coal, monetizable as LNG, and usable as feedstock.

This is the exact terrain SH-2050’s Gas-to-Shore framework was built for. Suriname is not a bystander to this trend; it is positioned to be a participant in it.

04 – Brazil Is Consolidating Its Position as an Atlantic Margin Technology Hub

Continued Petrobras activity — Pelotas concessions, Búzios subsea contracts, Helix service contracts — confirms Brazil’s trajectory as the dominant deepwater operator on the South Atlantic Margin. For Suriname, this matters directly: the same margin geology, the same FPSO ecosystem, and largely the same contractor base connect Brazil’s offshore sector to Guyana–Suriname Basin development. Brazil’s growth strengthens the regional supply chain Suriname depends on.

05 – Portfolio Optimization Is Not Decline

Reports of potential asset sales by supermajors and NOCs in the Permian — ExxonMobil, APA, Sinopec’s JV exit — should not be misread as retreat from hydrocarbons. This is capital recycling: mature assets are sold to private equity and specialist independents so capital can be redeployed toward higher-return opportunities elsewhere, including offshore frontier basins.

06 – Offshore Services Remain in Expansion Mode

Sustained activity from Petrobras, Ocean Installer, Oceaneering, Chevron, bpTT, and Helix indicates that offshore service capacity — vessels, subsea contractors, engineering firms — remains in active deployment rather than contraction. For Guyana and Suriname, this is favorable: the contractor base required for continued deepwater development remains experienced, available, and actively investing in capability.

07 – Licensing Rounds Are Still Opening, Not Closing

Egypt’s continuation of exploration licensing rounds, alongside similar moves elsewhere, signals that governments still view new acreage as an investment magnet, not a stranded liability. Suriname’s Open Acreage program — including Staatsolie’s Sector 2 (SHO East) proposal — sits squarely within this global pattern rather than against it.

08 – Logistics Has Become a Strategic Asset Class

A single order of nine VLCCs, worth roughly a billion dollars, illustrates how tightly oil markets now depend on tanker availability and export flexibility. Transport capacity is no longer a downstream afterthought; it is a strategic position in its own right.

GLIAG DOCTRINE

The next era of petroleum competition will be won less by discovering additional molecules than by controlling the infrastructure that converts, transports, stores, and monetizes those already discovered.

09 – What This Means for Suriname

Read against the Guyana–Suriname Basin, this season’s global pattern strengthens — rather than merely illustrates — several theses GLIAG has advanced for over a year:

- Gas-to-Shore gains relevance as gas infrastructure attracts global capital on the same footing as oil infrastructure.

- The New Modular Refinery becomes more defensible, precisely because downstream and conversion assets — not just upstream discovery — are drawing major institutional capital worldwide.

- Block 52’s dual-hydrocarbon portfolio gains strategic optionality in a market increasingly rewarding infrastructure flexibility over single-commodity exposure.

- GranMorgu should be read as an opening chapter, not a terminal achievement — the beginning of an industrial ecosystem rather than a single project milestone.

- Suriname’s long-term positioning should aim at becoming an integrated energy hub — production, gas monetization, refining, marine logistics, and petroleum intelligence — rather than a crude exporter awaiting the next discovery.

The chain from reservoir to republic does not end at first oil. It continues through every pipeline, terminal, refinery, and vessel that determines whether a discovery becomes durable national capability — or remains a number on a resource estimate.

This season’s global deal flow is not noise. It is a preview of the terrain Suriname is now entering.

Soso Lobi.

© 2026 GLIAG — Golden Lane Investments Advisory Group. Paramaribo · Delft.

petroleumenergyinsights.com

This essay is intended for strategic and educational purposes and does not constitute investment advice.