The Fourth Proposal

Sector 2: SHO EAST and the Quiet Repricing of the Guyana–Suriname Basin

GLIAG STRATEGIC BRIEF · JULY 2026 – Written by Marcel P. Chin-A-Lien, Petroleum & Energy Advisor – Founding Partner & Chief Architect GLIAG N.V. – Golden Lane Investments Advisory Group – A boutique group of senior advisors.

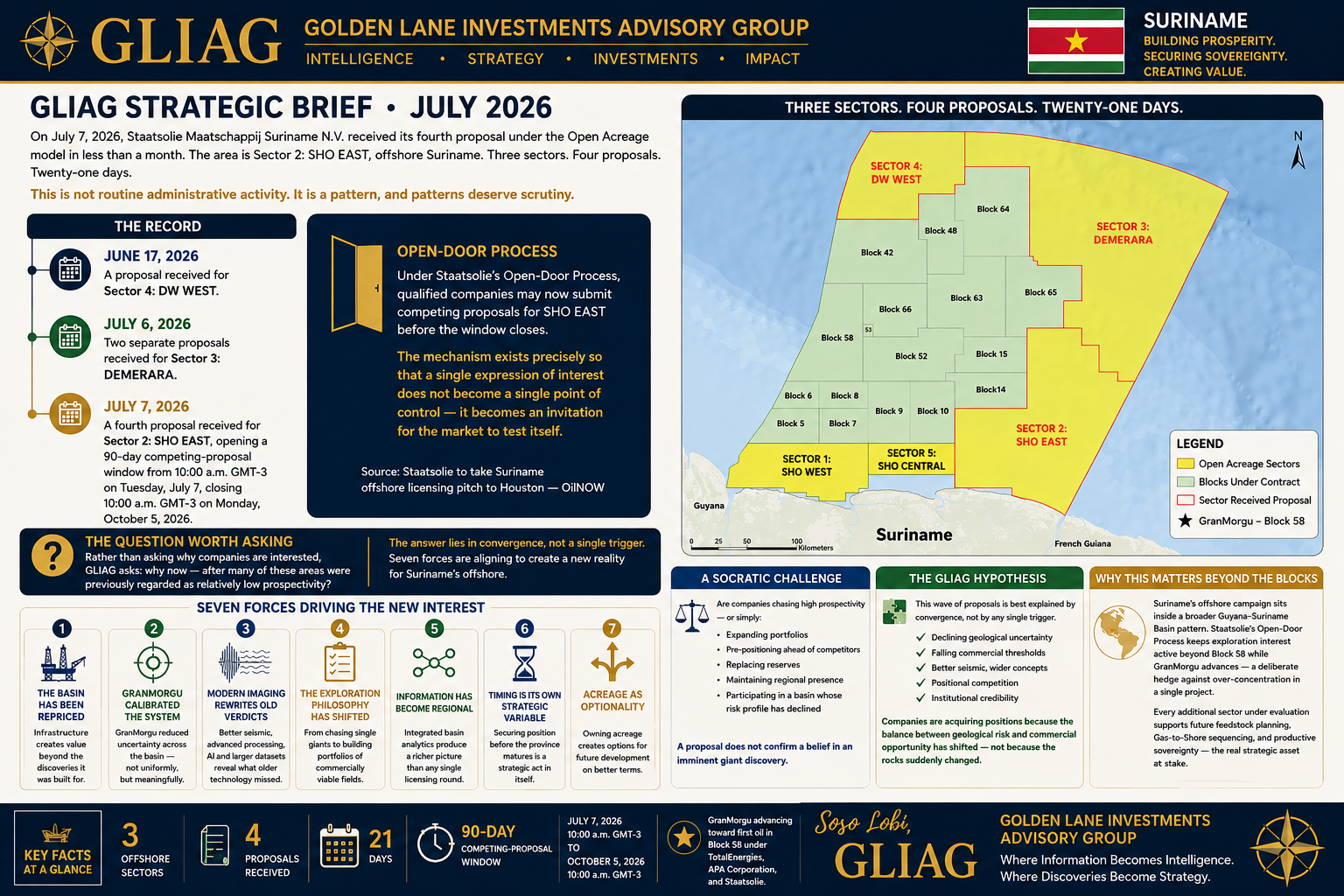

On July 7, 2026, Staatsolie Maatschappij Suriname N.V. received its fourth proposal under the Open Acreage model in less than a month. The area is Sector 2: SHO EAST, offshore Suriname. Three sectors. Four proposals. Twenty-one days.

This is not routine administrative activity. It is a pattern, and patterns deserve scrutiny.

The Record

- JUNE 17, 2026A proposal received for Sector 4: DW WEST.

- JULY 6, 2026 – Two separate proposals received for Sector 3: DEMERARA.

- JULY 7, 2026 – A fourth proposal received for Sector 2: SHO EAST, opening a 90‑day competing‑proposal window from 10:00 a.m. GMT‑3 on Tuesday, July 7, closing 10:00 a.m. GMT‑3 on Monday, October 5, 2026.

Under Staatsolie’s Open‑Door Process, qualified companies may now submit competing proposals for SHO EAST before the window closes. The mechanism exists precisely so that a single expression of interest does not become a single point of control — it becomes an invitation for the market to test itself.

Source: Staatsolie to take Suriname offshore licensing pitch to Houston — OilNOW

The Question Worth Asking

The obvious question is: why are companies suddenly interested in acreage that was, for years, regarded as peripheral? The more useful question is different. Rather than asking why companies are interested, GLIAG asks: why now — after many of these areas were previously regarded as relatively low prospectivity?

There is unlikely to be a single explanation. Several forces are converging at once.

1. The Basin Has Been Repriced

The rocks have not changed. The petroleum system has not changed. What has changed is the commercial risk. A decade ago, a 150–250 MMbbl discovery might have required its own standalone FPSO. Today, companies can reasonably contemplate future tie‑backs to infrastructure already committed or under construction. The threshold for commerciality has fallen — not because the geology improved, but because the economics did.

GLIAG DOCTRINE

Infrastructure creates value beyond the discoveries it was built for.

2. GranMorgu Calibrated the System

GranMorgu did more than prove oil. It recalibrated reservoir quality, migration pathways, charge timing, trap integrity, seal effectiveness, pressure regimes, drilling performance, and development cost benchmarks for the entire basin. Every successful well reduces uncertainty elsewhere — but only to the extent the geological analogy holds. The degree of risk reduction is not uniform across every structural setting and play type, and that unevenness is itself part of why some sectors are drawing proposals faster than others.

3. Modern Imaging Rewrites Old Verdicts

The “low prospectivity” label attached to many blocks reflected the technology of its era, not a permanent geological judgment. Broadband seismic, advanced depth migration, full‑waveform inversion, improved velocity models, AI‑assisted interpretation, and far larger regional datasets now exist. A prospect rejected in 2010 is not necessarily rejected in 2026.

4. The Exploration Philosophy Has Shifted

Twenty years ago, exploration targeted giants. Today, companies increasingly accept portfolios built from several medium‑sized accumulations, provided those accumulations can share infrastructure. The objective has moved from finding the single biggest field to maximizing the value of the whole portfolio.

5. Information Has Become Regional

No company evaluates one block in isolation anymore. Block 58, Block 52, Guyana’s producing developments, regional well results, published technical papers, seismic analogues, and basin modeling are now read as a single integrated dataset. That integration produces a richer picture than any single licensing round offered in the past.

6. Timing Is Its Own Strategic Variable

Offshore acreage is finite, and windows close. Waiting until multiple producing hubs are firmly established risks fewer available blocks, higher entry costs, and stronger competition. Acquiring position before the province fully matures is, in itself, a strategic act — independent of what any single well might find.

7. Acreage as Optionality

A company does not need to know today how a discovery will be developed. Owning acreage creates the option to develop it later, on terms shaped by whatever export systems, gas infrastructure, or additional FPSOs are added over the coming decade. Exploration, in this frame, is partly an investment in future flexibility rather than a bet on an imminent discovery.

A Socratic Challenge

It is worth questioning the opposite assumption as well. Are companies really moving because they believe SHO EAST or DEMERARA are highly prospective — or are there simpler explanations? A proposal under the Open‑Door Process may just as easily reflect portfolio expansion, reserve replacement, strategic pre‑positioning ahead of competitors, retention of an existing technical team’s regional presence, or participation in a basin whose overall risk profile has structurally declined. The act of submitting a proposal does not, by itself, confirm that a company expects an imminent giant discovery.

Nor should the sequencing itself be over‑read. The first proposal under a given round can act as a signal that draws attention to an area, prompting competitors to revisit their own regional evaluations before an exclusivity window closes. That can create a cascade of independent reassessments that looks, from the outside, like coordinated conviction — when it may simply be several companies arriving at similar conclusions on similar timelines, using similar data.

The GLIAG Hypothesis

From a GLIAG perspective, the current wave of proposal activity is best explained by convergence, not by any single trigger:

- Declining geological uncertaintyNew discoveries and improved basin understanding have narrowed the range of outcomes companies must price into their evaluations.

- Falling commercial thresholdsPlanned and committed infrastructure increases development flexibility, making previously marginal acreage newly viable.

- Better seismic, wider conceptsImproved acquisition and interpretation have expanded the range of exploration plays companies are willing to pursue.

- Positional competitionCompanies are securing acreage ahead of full basin maturity, when terms are still favorable and competition is thinner.

- Institutional credibilitySuriname’s licensing framework and Staatsolie’s process discipline have reduced above‑ground risk, which is itself a component of investment decisions.

The most important insight may be this: companies are not necessarily chasing SHO EAST, DEMERARA, or DW WEST because these sectors suddenly became “high prospectivity” in a geological sense. They may be acquiring positions because the balance between geological risk and commercial opportunity has shifted enough that acreage once set aside now warrants a second look. That distinction is subtle. Its implications for how Suriname’s offshore province evolves over the next decade are not.

Three offshore sectors. Four proposals. Twenty‑one days. A 90‑day competing‑proposal window now runs to October 5, 2026 — while GranMorgu advances toward first oil in Block 58 under TotalEnergies, APA Corporation, and Staatsolie.

Why This Matters Beyond the Blocks

Suriname’s offshore campaign does not exist in isolation. It sits inside a broader pattern of industry interest across the Guyana–Suriname Basin, where discoveries in Guyana have already scaled into large production and Suriname is working to bring its own first offshore development on stream. Staatsolie’s Open‑Door Process is one way of keeping exploration interest active beyond Block 58 while GranMorgu advances — a deliberate hedge against the risk that all national attention, and all national exposure, concentrates in a single project.

For a country moving from an Exploration Economy toward a Conversion Economy, that hedge matters. Every additional sector under active evaluation is a data point for future feedstock planning, for Gas‑to‑Shore sequencing, and for the kind of productive sovereignty GLIAG has argued is the real strategic asset at stake — not any single well, but the accumulating optionality of the basin as a whole.

Soso Lobi,

GLIAG — Golden Lane Investments Advisory Group

Where Information Becomes Intelligence. Where Discoveries Become Strategy.