| GOLDEN LANE INVESTMENTS ADVISORY GROUPG L I A G ◆ petroleumenergyinsights.com WHY A NEW REFINERY IN SURINAMEIS A PROFITABLE INVESTMENTDESPITE THE INDUSTRY’S THIN MARGINS A GLIAG Essay for Decision-MakersFundamentals, Structural Differentiators, and the Bankability Case Drs. M. P. T. Chin-A-Lien, MBA, M.Sc., Ing.Founding Partner & Chief ArchitectGolden Lane Investments Advisory Group – CPG Nr. 5201-1996 (AAPG) │ CEurGeol Nr. 92-1996 (EFG) │ AIEN Energy Negotiator |

| REFERENCE │ GLIAG-ESSAY-SUR-REF-004-2026Companion to GLIAG-MA-SUR-REF-003-2026 │ GLIAG-TOR-SUR-REF-001-2026Series: A New Modular Refinery for Suriname (GLIAG-WP-2026-REF-001)5 July 2026 │ Confidential │ Soso Lobi |

| GLIAG ◆ Golden Lane Investments Advisory Group | GLIAG-ESSAY-SUR-REF-004-2026 │ 5 July 2026 |

The Question, Stated Honestly

Any sophisticated reader who has followed global refining over the past decade will raise the same objection when the words “new refinery” are pronounced: the margins are gone.Rotterdam and Singapore complex crack spreads have retreated from the extraordinary 2022 highs of $30-plus per barrel to a structurally compressed $4–8 / bbl range. Wood Mackenzie’s global composite utilisation averaged roughly 75 percent in 2024 — a level that historically barely covers fixed OPEX. New capacity from Dangote (650 kbpd), Al Zour (615 kbpd), Duqm and Dos Bocas has added ~ 1.5 million bpd of throughput since 2022. Europe is closing refineries, not building them.

If this is the industry, why build a new one in Suriname?

The answer is that the low-margin critique is entirely correct — and entirely inapplicable to the project GLIAG has designed. It applies to merchant refineries competing in open product markets for discretionary throughput. It does not apply to a captive-market, import-substitution refinery with sovereign feedstock guarantee, near-zero crude freight, and domestic pricing at full import parity. The two economics are not variations of one another; they are different businesses.

The Fundamentals — What Determines Refinery Profitability

A refinery’s profitability is not the crack spread. It is the Net Refining Margin (NRM) — the gross margin, less feedstock cost differential, less fixed operating cost per barrel, less capital recovery per barrel. Four levers determine whether a refinery earns its cost of capital:

◆ Feedstock cost basis. Merchant refineries buy crude at spot plus freight. Their variable cost is 75–85 percent of total operating cost, and they have no structural advantage over any competitor buying the same barrel.

◆ Product realisation. Merchants sell into open markets and take the marginal-barrel price. They are price-takers with no floor.

◆ Utilisation. Below roughly 80 percent, fixed costs strand capital recovery. The industry has been operating close to that threshold for three years.

◆ Capital intensity. A 300,000 bpd greenfield complex refinery in the Middle East costs $6–8 billion — $20,000–27,000 per bpd of capacity. At compressed crack spreads, that capital cannot be recovered.

Every one of these four levers is inverted in Suriname’s favour.

Why Suriname Is Structurally Different

Five Advantages, Quantified

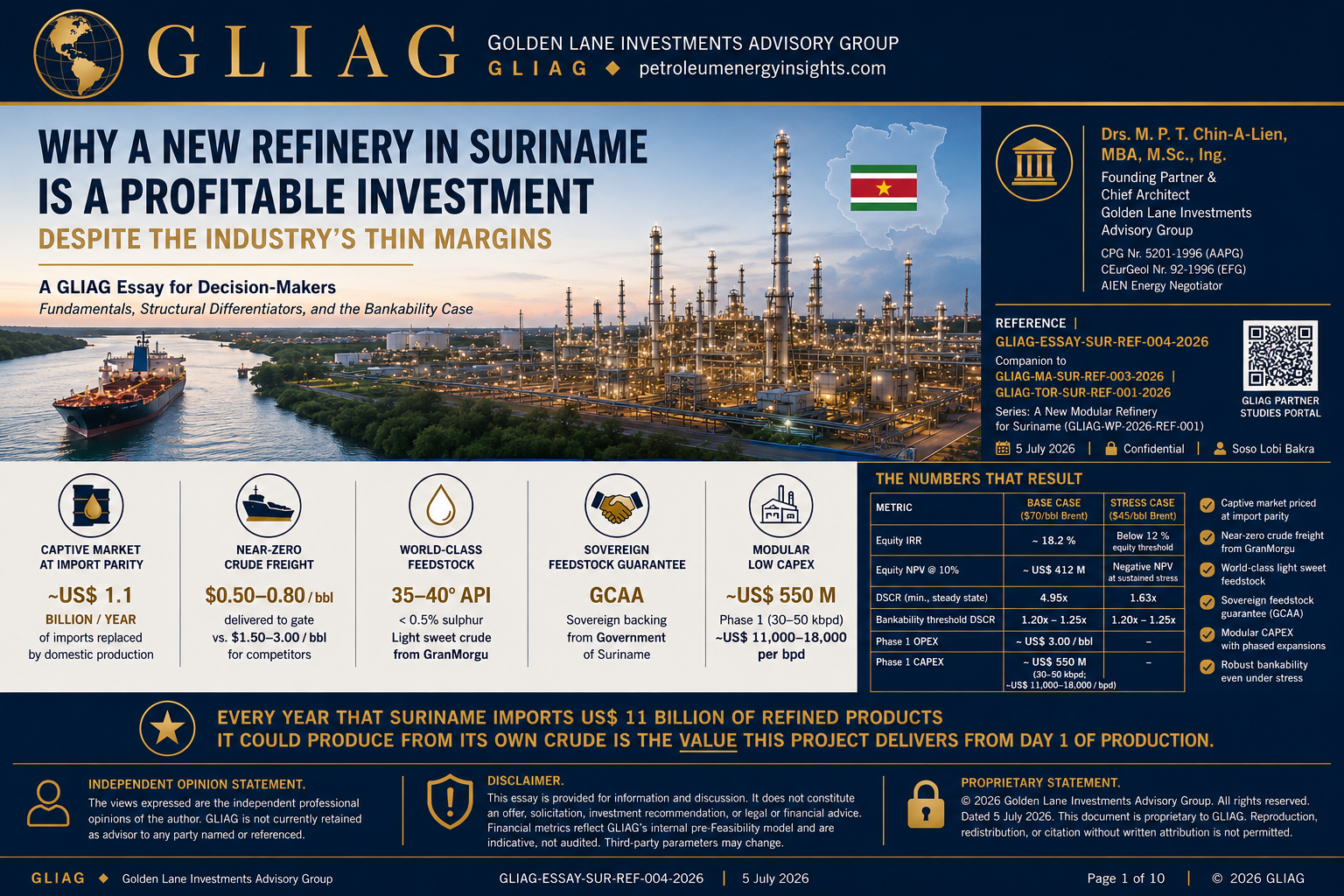

1. A captive domestic market, priced at import parity

Suriname currently imports approximately 17,000 bpd of refined products at a cost of ~ US$ 1.1 billion per year in foreign exchange. The existing Tout Lui Faut refinery — 15,000 bpd nameplate, running at roughly 50 percent utilisation on Saramacca medium-heavy crude — produces no jet fuel, no IMO 2020-compliant bunker fuel, and no EN590 automotive diesel. Every barrel of gasoline, jet, and ULSD the new refinery produces displaces an imported barrel and can be priced at landed import parity — CIF Rotterdam or Houston, plus freight, insurance, port fees and trader margin.

| Refineries serving the domestic market in a net-importing country may be able to charge import-parity prices, which include freight costs which the domestic refinery is not incurring.— World Bank, empirical finding |

For Suriname, the Rotterdam-to-Paramaribo product freight differential alone is $3–5 / bbl — US$ 18.6–31 million per yearof structural margin before any other advantage is counted.

2. Near-zero crude freight — a GranMorgu tie-in

Every non-integrated merchant refinery bears crude freight from origin to gate. Block 58 lies ~ 150 km offshore Paramaribo. Shuttle-tanker or dedicated tie-in delivery to the 220-hectare Suriname River site costs approximately $0.50–0.80 / bbl, versus $1.50–3.00 / bbl for competing Atlantic Basin refineries importing Middle East or West African grades. At 50,000 bpd Phase 1 throughput, this is US$ 18–45 million per year of structural cost advantage, independent of the global margin environment.

3. A world-class feedstock — GranMorgu light sweet crude

GranMorgu (~ 35–40° API, < 0.5 % sulphur, low TAN) is the opposite of the global refining margin problem. A modular hydroskimming / hydrotreating configuration with a Nelson Complexity Index of roughly 5.5–6.5 achieves the product-slate value that would require an NCI 9–11 refinery on heavier crudes. The project consumes less energy per barrel, produces less residue, requires no expensive residue-upgrading unit, and delivers a higher-value product yield per barrel of crude processed.

The 1 October 2024 Final Investment Decision by TotalEnergies (40 %), APA Corporation (40 %) and Staatsolie (20 %) — supported by a US$ 1.6 billion syndicated mini-perm led by Afreximbank, Bladex and Deutsche Bank across 18 lenders — has removed feedstock supply risk from the domain of speculation. First oil is scheduled for 2028.

4. Sovereign feedstock guarantee — the Government Crude Allocation Agreement

The GLIAG project structure includes a Government Crude Allocation Agreement (GCAA) between the Republic of Suriname (through the Ministry of Natural Resources and Staatsolie N.V.) and the refinery SPV. The GCAA grants the refinery a defined term volume of Staatsolie’s Block 58 equity crude entitlement (44,000 bpd gross at plateau) at Brent less a quality adjustment, netted back to the Suriname River terminal, over a tenor matching senior debt (15–18 years).

From a lender’s perspective, the GCAA is not a commercial supply contract. It is a sovereign obligation, backed by a PSC with two publicly traded international oil companies. It converts feedstock risk into an investment-grade counterparty exposure — the exact instrument that makes the project bankable to DFC, IDB Invest, IFC and Afreximbank, and which existing Caribbean refineries (Curaçao Isla, Petrojam) have historically lacked.

5. Modular CAPEX — an order of magnitude below greenfield complex

The Phase 1 configuration is 30,000–50,000 bpd at approximately US$ 550 million CAPEX (~ US$ 11,000–18,000 per bpd) — roughly half the per-barrel capital intensity of a large greenfield complex. Factory-prefabricated modular construction shortens the schedule and reduces execution risk. Phase 2 and Phase 3 expansions are financed from Phase 1 operating cash flow, avoiding the upfront capital burden that destroys merchant-refinery economics at today’s crack spreads.

The Numbers That Result

The GLIAG financial model — a 120-scenario Monte Carlo grid across six oil-price cases ($45–$120 / bbl Brent), three phases, and variable feedstock volumes — produces the following headline metrics under a base-case $70 / bbl Brent, 50,000 bpd Phase 1 throughput:

| Metric | Base case ($70/bbl Brent) | Stress case ($45/bbl Brent) |

| Equity IRR | ~ 18.2 % | Below 12 % equity threshold; senior debt still serviceable |

| Equity NPV @ 10 % | ~ US$ 412 M | Negative NPV at sustained stress |

| DSCR (min., steady state) | 4.95x | 1.63x |

| Bankability threshold DSCR | 1.20x – 1.25x | 1.20x – 1.25x |

| Phase 1 OPEX | ~ US$ 3.00 / bbl | — |

| Phase 1 CAPEX | ~ US$ 550 M (30–50 kbpd; ~ US$ 11,000–18,000 / bpd) | — |

For context, the sector average DSCR for project-financed power generation is 1.30x–1.50x; for merchant refineries with no sovereign offtake, lenders require 1.50x–2.00x minimum. The GLIAG project clears that bar with an order-of-magnitude margin at base case and remains debt-serviceable even at a $45 / bbl sustained Brent stress — a scenario well below any plausible medium-term price given OPEC+ management and current geopolitical dynamics.

The Correct Benchmark

The single most important analytical correction in the Suriname refinery debate is the choice of benchmark. The objection that “global refining margins are too low” applies a Rotterdam or Singapore crack spread to a project that does not sell into Rotterdam or Singapore. The correct benchmark is not the crack spread. It is the import-parity margin — the difference between the landed CIF cost of imported refined products in Paramaribo and the delivered cost of domestically refined products from indigenous crude. That difference is durable, structural, and independent of the global merchant-refinery cycle. It is, in the analytically precise sense of the term, a value-in-place measurement.

| THE PLAIN ARITHMETICEvery year that Suriname continues to import US$ 1.1 billion of refined products it could produce domestically from its own crude is a direct measure of the value this project delivers from Day 1 of production. |

Conclusion — A Different Business, Correctly Priced

Global merchant refining is a mature, oversupplied, margin-compressed industry with declining strategic returns. That reality is not in dispute, and no responsible advisor should suggest otherwise. But it is not the industry Suriname is entering.

The GLIAG Suriname Modular Refinery is an import-substitution infrastructure asset with a sovereign feedstock guarantee, a captive domestic market priced at import parity, near-zero crude freight, world-class light sweet feedstock, and modular CAPEX. It is closer in economic character to a regulated utility with a take-or-pay offtake than to a merchant refinery — and it should be priced, financed, and defended as such.

Suriname will spend the next twenty-five years converting deepwater discoveries into national wealth. Doing so while importing US$ 1.1 billion of refined products every year is not a strategy — it is an omission. This refinery closes it.

References & GLIAG Studies Register

This essay draws on two bodies of source material: (i) GLIAG’s proprietary Suriname Refinery study programme — the bankability, pre-feasibility, financial-modelling, white-paper and strategic-entry work produced under the flagship reference GLIAG-WP-2026-REF-001; and (ii) a curated set of published, independently authored references from the IEA, Wood Mackenzie, McKinsey, the U.S. EIA, Concawe, Carbon Tracker, BP, and the world’s leading energy-press sources on refining margins. Every quantitative claim in the essay is traceable to one of the two.

A. GLIAG Studies Register — Suriname New Modular Refinery Programme

The following GLIAG works form the analytical corpus supporting this essay. All are proprietary to Golden Lane Investments Advisory Group and are available to qualified counterparties under Non-Disclosure Agreement.

Flagship white paper

◆ GLIAG-WP-2026-REF-001 — “A New Modular Refinery for Suriname: A Strategic SH-2050 Conversion Platform for Energy Security, Industrialization and National Wealth Creation” (GLIAG, 2026).

Strategic and policy studies

◆ GLIAG-SES-SUR-001-2026 — Strategic Entry Studies, Complete Edition (225 pp.; sector positioning, upstream–downstream integration, macro linkages).

◆ GLIAG_Complete_Study_Programme_Suriname_New_Refinery — master programme index and study-by-study cross-reference (GLIAG, 2026).

◆ GLIAG_Voorbij_MOP_2027–2031_NL_DEFINITIEF— Dutch-language strategic review, “Beyond the MOP 2027–2031” (GLIAG, 2026).

Pre-feasibility and technical studies

◆ GtS_PreFS_Suriname_GLIAG_2026 — Pre-Feasibility Study, refinery + Gas-to-Shore integration (GLIAG, 2026).

◆ GLIAG-TOR-SUR-REF-001-2026 — Terms of Reference, refinery development and advisory scope (GLIAG, 2026).

Bankability and financial studies

◆ GLIAG_Bankability_Analysis — Bankability analysis (DOCX and PDF releases, GLIAG, 2026).

◆ GtS_VolV_DSCR_Bankbaarheid_Rev26 — DSCR and bankability, Volume V, Dutch-language edition (GLIAG, 2026).

◆ GLIAG_Refinery_Financial_Model_Summary.xlsx — 120-scenario Monte Carlo grid: 6 Brent cases ($45–$120 / bbl), 3 phases, variable feedstock (GLIAG, 2026).

◆ GLIAG-MA-SUR-REF-003-2026 — Refinery Margin Analysis: the five structural differentiators framework (GLIAG, 4 July 2026).

DFI, investor and stakeholder communication

◆ GLIAG_DFC_White_Paper_Modular_Refinery_Suriname — White paper prepared for U.S. International Development Finance Corporation review (GLIAG, June 2026).

◆ GLIAG_Refinery_Investor_Deck_Rev26 — Investor deck, English / Nederlands / Sranan Tongo editions (GLIAG, 2026).

◆ GLIAG-ESSAY-SUR-REF-002-2026 — Strategic Investment Essay, prior release (GLIAG, 2026).

◆ GLIAG-Refinery-Dashboard — interactive web application, live model outputs and scenario browser (GLIAG, 2026).

B. Trusted External References on Refinery Margins

The published sources below — all independent of GLIAG — corroborate the margin, utilisation, capacity-closure and outlook data cited in this essay. Institutional lenders (DFC, IDB Invest, IFC, Afreximbank, KfW) routinely use the same sources for their own refining-sector due diligence.

International Energy Agency (IEA)

◆ IEA, Oil Market Report — March 2025 (global refinery margins, throughput and product balances).

◆ IEA, Oil Market Report — November 2024.

Wood Mackenzie

◆ Wood Mackenzie, Global refinery closure outlook to 2035— 101 of 420 global refineries at risk of closure by 2035; 18.4 million bpd = ~ 21 % of capacity.

◆ Wood Mackenzie, Weekly Refining Margins: bump along the floor — composite margins ~ $5.17 / bbl in 2024.

◆ Wood Mackenzie, Balancing refining, chemicals and retail to optimise future performance — Net Cash Margin outlook: $4.3 / bbl (2025) to $6.4 / bbl (2030).

◆ Reuters (citing Wood Mackenzie), Global oil refiners see short-term boost from higher margins, 3 June 2025 — June 2025 margins $8.37 / bbl vs. $33.50 / bbl in June 2022.

◆ DieselNet, Wood Mackenzie: 21 % of global refining capacity faces closure threat (April 2025).

McKinsey & Company

◆ McKinsey, The near-term outlook for refining: where to now?.

◆ McKinsey, Global Energy Perspective 2023 — Refining outlook.

◆ McKinsey, Refining in the energy transition through 2040.

◆ McKinsey, The conundrum of new complex refining investments — quoted verbatim in the GLIAG Margin Analysis regarding structurally flat post-2009 margins.

◆ Rigzone (citing McKinsey), Overall profitability of oil & oil-products decreased in 2024, 4 March 2025.

U.S. Energy Information Administration (EIA)

◆ EIA, Today in Energy — Refinery margins, 3Q 2025.

◆ EIA, STEO Petroleum Refining Model (3-2-1 crack-spread methodology).

Carbon Tracker, Concawe & BP

◆ Carbon Tracker Initiative, Margin Call: Refining Capacity in a 2 °C World.

◆ Concawe / Wood Mackenzie (Christopher Barry), NWE refining margins forecast — Keynote Presentation.

◆ BP, Statistical Review of World Energy (regional refining margin history).

World Bank

◆ World Bank, Refinery Economics in Developing Countries— empirical finding on import-parity pricing for refineries in net-importing countries (source of the pull-quote on p. 3).

Suriname / Guyana project references

◆ TotalEnergies, Suriname: TotalEnergies announces Final Investment Decision on GranMorgu, 1 October 2024.

◆ Staatsolie Maatschappij Suriname, TotalEnergies and APA Corporation announce Final Investment Decision for Block 58.

◆ LatinFinance, Loan of the Year 2025 — Block 58 GranMorgu US$ 1.6 bn syndicated mini-perm.

◆ OilNOW, GranMorgu moves from blueprint to buildout as Suriname targets first oil.

Industry cost benchmarks

◆ Compass International, Refinery CAPEX and OPEX Benchmarks (2024 edition) — modular / greenfield per-bpd cost intervals used to calibrate the GLIAG Phase 1 estimate.

◆ S&P Global Commodity Insights / Platts, Global Refining Margin Assessments — subscription database used for daily crack-spread benchmarking.

Marcel P. T. Chin-A-Lien

Petroleum & Energy Advisor

Founding Partner & Chief Architect, Golden Lane Investments Advisory Group

Drs., MBA, M.Sc., Ingeniero Geólogo │ CPG Nr. 5201-1996 (AAPG) │ CEurGeol Nr. 92-1996 (EFG) │ AIEN Energy Negotiator (June 2021)

Independent Opinion Statement. The views expressed are the independent professional opinions of the author. GLIAG is not currently retained as advisor to any party named or referenced.

Disclaimer. This essay is provided for information and discussion. It does not constitute an offer, solicitation, investment recommendation, or legal or financial advice. Financial metrics reflect GLIAG’s internal pre-Feasibility model and are indicative, not audited. Third-party parameters may change.

Proprietary Statement. © 2026 Golden Lane Investments Advisory Group. All rights reserved. Dated 5 July 2026. This document is proprietary to GLIAG. Reproduction, redistribution, or citation without written attribution is not permitted.

| Why a New Refinery in Suriname Is a Profitable Investment | Page of │ © 2026 GLIAG |