Predictive Exploration™ Series

Marcel Chin-A-Lien – February 2026

Petroleum & Energy Insights Advisor

Co-founder, Golden Lane Investments Advisory Group

Executive Overview

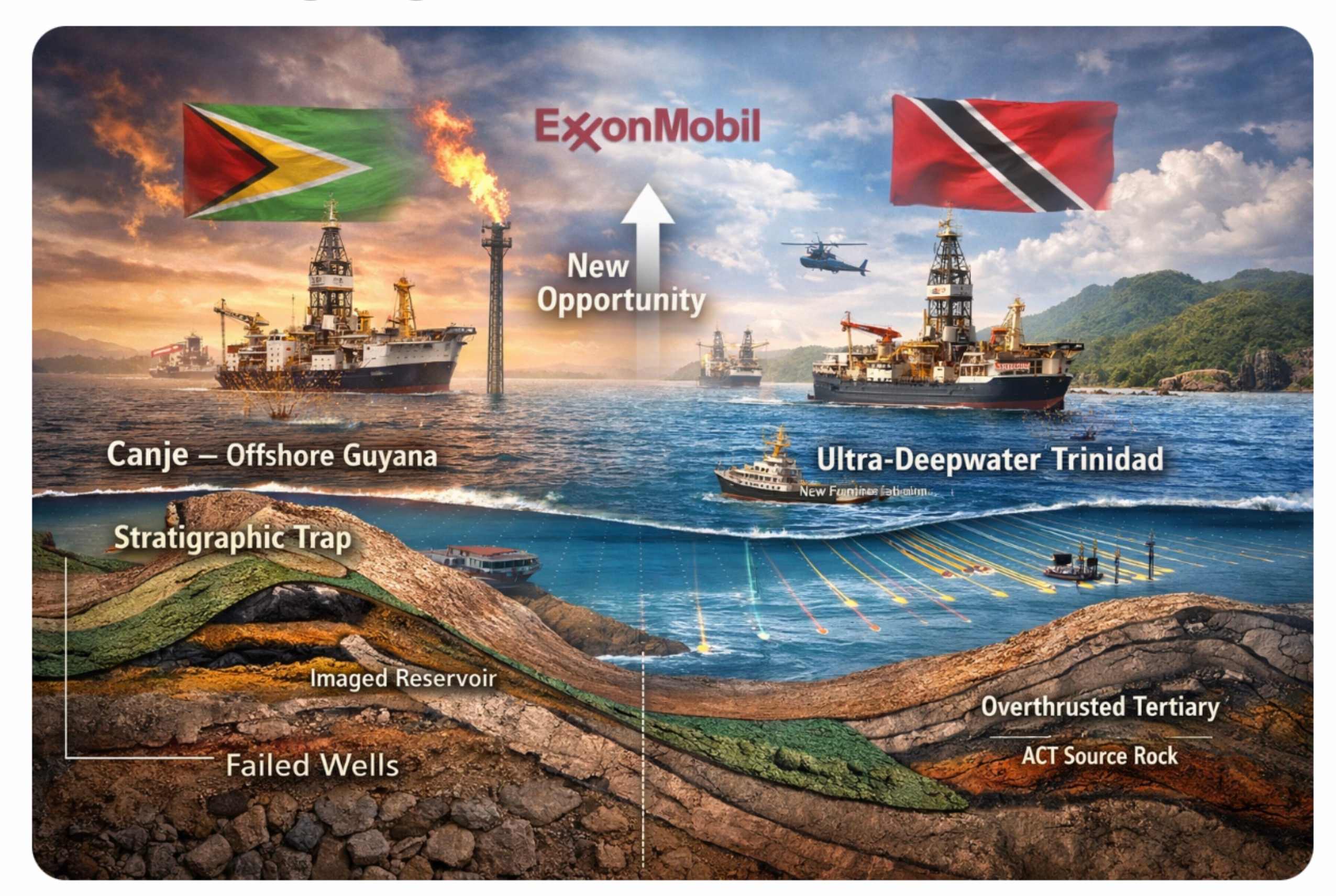

ExxonMobil’s apparent pivot from the Canje Block (Guyana) toward Ultra-Deepwater 1 (UD-1) offshore NE Trinidad is not a geological contradiction.

It is a capital allocation decision shaped by stratigraphic trap performance, ultra-deepwater cost thresholds, and portfolio optionality.

Canje is not geologically dead.

The drilled wells demonstrate working petroleum system elements.

However, no commercial development anchor has yet emerged.

UD-1 represents early-cycle optionality where large-scale seismic de-risking precedes drilling.

1. The Canje Record: Robust Geological Testing

- Bulletwood-1: 2,846 m water depth; TD 6,690 m; confirmed seismic interpretation; evidence of non-commercial hydrocarbons. (JHI Associates)

- Jabillo-1: 2,903 m water depth; TD 6,475 m; Upper Cretaceous strat trap objective; no commercial discovery declared. (Investegate)

- Sapote-1: 2,549 m water depth; TD 6,758 m; Upper Cretaceous strat trap objective; non-commercial hydrocarbons reported in deeper target. (Offshore Energy)

Conclusion: Charge exists. Reservoir exists. Commercial trap robustness remains unproven.

2. Why Canje Becomes Economically Sensitive

Ultra-deepwater amplifies geological imperfection. At ~2.5–2.9 km water depth and ~6.5–6.8 km TD:

- Well cost escalates dramatically

- Operational risk increases

- Minimum commercial size rises

After three non-commercial outcomes, marginal probability of success must improve materially to justify another nine-figure well.

3. Why Exxon Moves to NE Trinidad (UD-1)

- UD-1 consolidates seven blocks.

- Water depths: 2,000–3,000 m.

- ~6,000 km² 3D seismic contracted before drilling. (Reuters)

- Exxon signaled regional leverage from Guyana experience. (Reuters)

Interpretation: Exxon is buying information before drilling. Canje is post-drill refinement. UD-1 is pre-drill portfolio generation.

4. Canje vs UD-1 Decision Tree

Illustrative capital allocation logic: late-cycle refinement versus early-cycle optionality.

5. Probability of Success vs Expected Monetary Value

EMV = PoS × NPVsuccess − Well Cost

This sensitivity illustrates why declining PoS after multiple non-commercial wells compresses expected value unless discovery size is very large.

Socratic Dialogue Sidebar

Socrates: If Canje shows hydrocarbons, why leave?

Student: Because they are not commercial.

Socrates: Is that geology or economics?

Student: Both. Ultra-deepwater punishes modest columns.

Socrates: Then why Trinidad?

Student: Because seismic first buys knowledge before drilling.

Socrates: So the move is not from “bad basin” to “good basin”?

Student: It is from late-cycle refinement to early-cycle optionality.

Balanced Conclusion

Canje is a technically working petroleum system lacking a commercial anchor. Its future requires a materially improved geological thesis.

UD-1 is frontier geology with large option value and seismic-first de-risking.

The pivot reflects capital discipline, not geological abandonment.

References

- JHI Associates – Bulletwood-1 Results

- Investegate – Jabillo & Sapote Reporting

- Offshore Energy – Sapote-1

- Reuters – UD-1 Seismic Contract

- Reuters – UD-1 Award & Strategic Framing

About the Author

Marcel Chin-A-Lien is a Global Petroleum & Energy Advisor with 48 years of international experience spanning giant field discovery, upstream M&A, PSC design, fiscal optimisation, and government negotiation.

He integrates petroleum systems analysis with commercial strategy, investment realism, and contract architecture to align geology with capital discipline.

Certified Petroleum Geologist (AAPG #5201) | Chartered European Geologist (EFG #92) | Energy Negotiator (AIEN)

Contact: marcelchinalien@gmail.com