Gas Architecture, Sovereign Strategy & Long-Term Value Creation for Suriname

Executive Overview

Written by Marcel Chin-A-Lien – Petroleum & Energy Advisor – 22 February 2026.

Sloanea is not merely a gas discovery.

It is a strategic inflection point.

The core decision facing Suriname is not whether gas exists.

It is how that gas should be deployed.

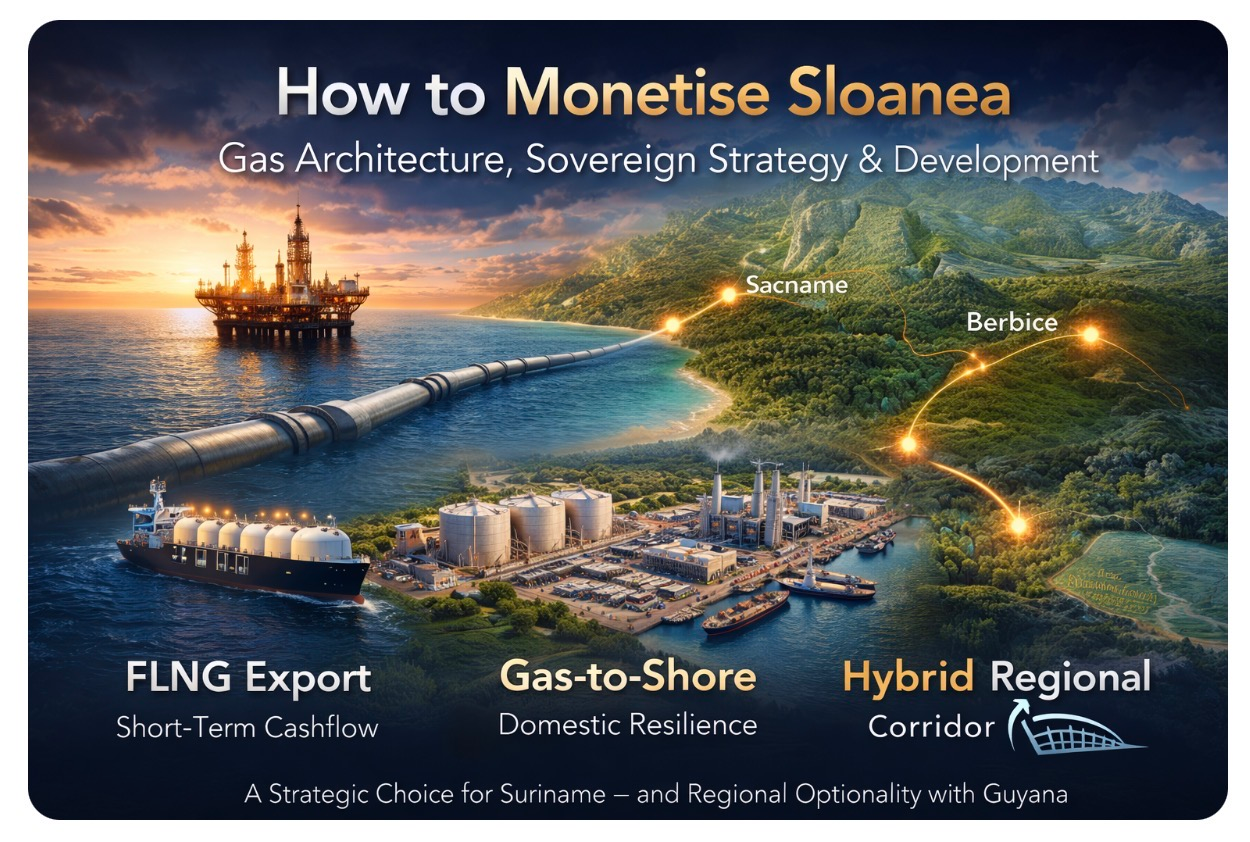

Three monetisation pathways emerge:

- Full FLNG Export Model

- Gas-to-Shore (GtS) using 20% Domestic Entitlement

- Hybrid / Regional Gas Architecture (Suriname–Guyana integration)

The question is not technical feasibility alone.

It is institutional design, capital discipline, fiscal resilience, and long-term development architecture and wise energy strategy

Executive Comparative – Sloanea Monetisation Options

| Dimension | FLNG Only | Gas-to-Shore (20%) | Hybrid / Regional Hub |

|---|---|---|---|

| Indicative NPV (US$ million) | ~4,200 | ~2,800 | ~3,500 |

| IRR (project level) | 18–22% | 13–16% | 15–18% |

| Domestic Energy Security | Low | High | Very High |

| Industrial & Regional Development | Limited | Strong (Nickerie anchor) | Transformational (Berbice corridor) |

| Financeability | Very Strong | Conditional (firm supply + PPA) | Complex multi-party |

| Key Fragility | Lower | Utilisation risk | Treaty + governance complexity |

The Strategic Value of Gas-to-Shore

While FLNG maximises short-term capital efficiency, Gas-to-Shore maximises long-term sovereign resilience.

1. Energy Cost Transformation

- Reduction of heavy fuel oil dependency

- Lower and more stable electricity tariffs

- Improved macroeconomic predictability

2. Industrial Anchoring – Nickerie Development

- Agro-processing clusters

- Cold storage logistics

- Light manufacturing and fabrication services

- Local services ecosystem growth

3. Regional Integration – Berbice Corridor

High-level discussions between Suriname and Guyana have already acknowledged the strategic value of cross-border energy integration. A pipeline interconnection increases:

- Security of supply

- Infrastructure utilisation

- Investment attractiveness

- System redundancy

The Critical Questions??

- Is 20% entitlement firm enough to underpin take-or-pay contracts?

- Can domestic demand ramp-up synchronise with offshore plateau?

- Is tariff governance transparent and predictable?

- Does institutional capacity match project complexity?

- Would blended finance lower WACC sufficiently?

If alignment holds, Gas-to-Shore becomes a development engine. If sequencing fails, it becomes a fiscal burden.

Balanced Conclusion

Gas does not create development automatically. Architecture does.

The most prudent sovereign pathway appears sequential:

- Stabilise via export-led cashflow (FLNG)

- Secure firm domestic tranche

- Build Phase 1 Gas-to-Shore conservatively sized

- Scale regionally once contractual and institutional maturity is proven

The objective is not export versus domestic use.

It is disciplined integration.

About the Author

Marcel Chin-A-Lien

Global Petroleum & Energy Advisor

Nearly five decades of international experience integrating exploration, production strategy, fiscal regime design, and commercial structuring across mature and frontier basins.

- Drs – Petroleum Geology

- Engineering Geologist – Petroleum

- Executive MBA – International Business & Petroleum

- MSc – International Management

- Certified Petroleum Geologist (AAPG)

- Chartered European Geologist (EFG)

Strategic focus: Exploration Strategy • PSC Design • Fiscal Optimisation • Sovereign Advisory • M&A • Integrated Technical-Commercial Structuring

Golden Lane Investments Advisory Group

Strategic Energy Advisory | Sovereign Fiscal Modelling | Integrated Gas Architecture

For advisory engagement:

Email: marcelchinalien@gmail.com

LinkedIn: Marcel Chin-A-Lien