Integrated Economic and Fiscal Assessment

Independent Benchmark Modelling Under Stated Assumptions

Marcel Chin-A-Lien

Petroleum & Energy Advisor (Independent)

18 February 2026

Important Disclaimer and Scope Clarification

This publication presents my own independent analytical modelling exercise prepared in a private professional capacity.

It is most certainly not an official statement of the Government of Suriname, Staatsolie Maatschappij Suriname N.V., or any other regulatory authority.

The Block 58 Production Sharing Contract (PSC) is not publicly disclosed.

Accordingly, Suriname fiscal mechanics presented herein are based on a Model PSC proxy framework, constructed from publicly available structural parameters and professional inference.

All results depend entirely on stated assumptions regarding production profile, capital expenditure, operating expenditure, oil price, discount rate, and fiscal structure.

Comparative references are structural illustrations only and do not imply normative ranking.

1. Executive Summary

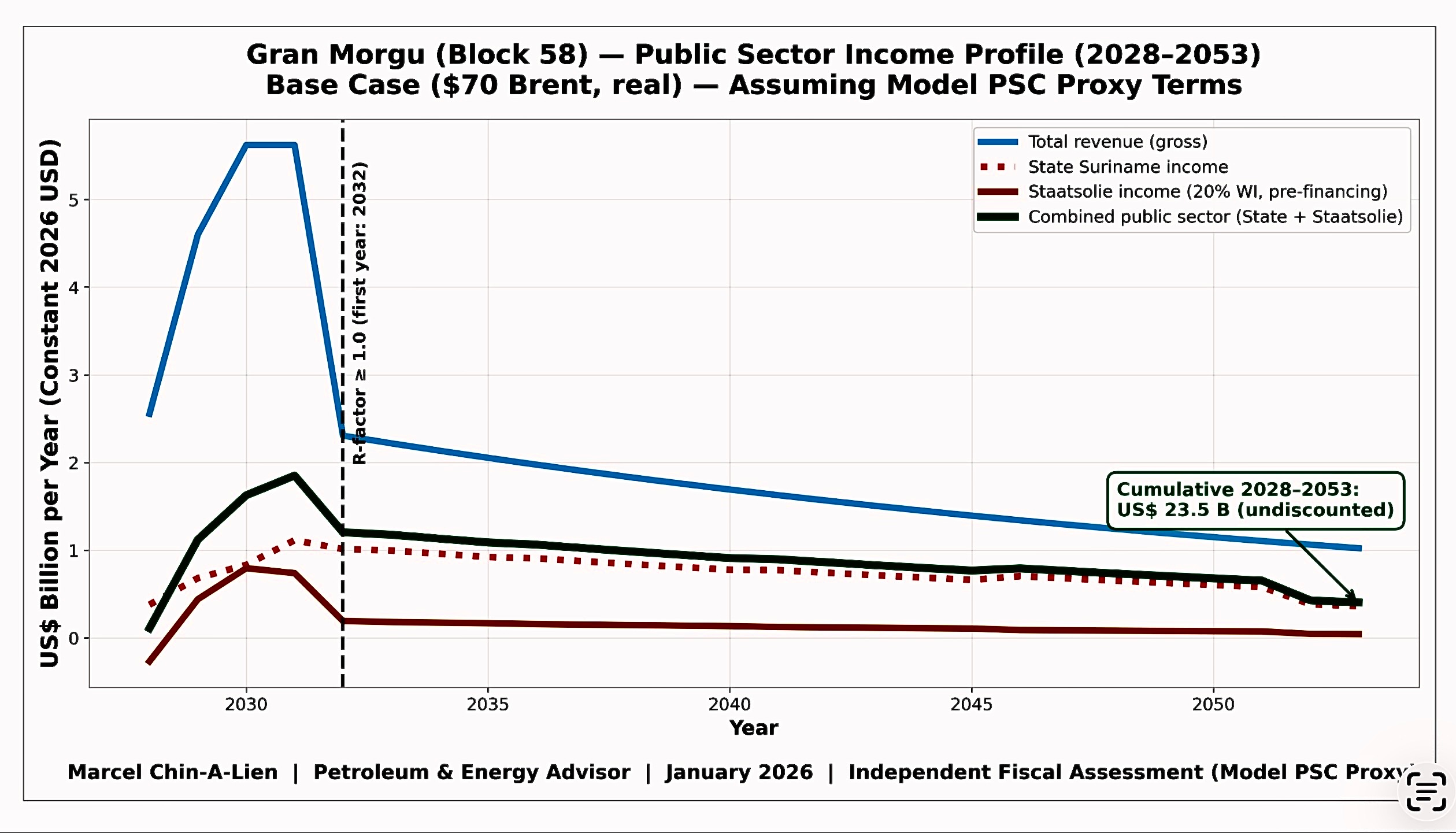

This report presents my own, independant consolidated economic and fiscal analysis of the Gran Morgu development (Block 58 offshore Suriname) over the assumed economic production life 2028–2053 (25 years).

Base Case Assumptions (Constant 2026 USD)

- Production life: 2028–2053

- Cumulative production (modelled): ~760 MMbbl

- CAPEX: US$ 10.5 billion

- OPEX (proxy): ~US$ 10/bbl

- Oil price: US$ 70 Brent (real)

- Discount rate: 10% real

Base Case Results

- Total gross revenue: US$ 53.2 billion

- Total public sector cash (State + Staatsolie): US$ 23.5 billion

- Life-of-project public share of gross revenue: 44.2%

- NPV10 public take (net project basis): ~73%

- Contractor IRR (real, proxy): ~18–19%

All values are model outputs under stated assumptions and are fully reproducible.

2. Fiscal Modelling Framework

Suriname – Model PSC Proxy Structure

- Royalty: 6.25%

- Cost recovery ceiling: 80%

- Income tax: 36%

- Profit oil allocation via R-factor mechanism

- State participation: 20% via Staatsolie (pre-financing cash shown)

Cashflow order: Royalty → Cost Recovery → Profit Oil → Income Tax → Participation.

3. Public Version Core Visual

For public transparency, the primary revenue profile is presented below. All additional figures, annual tables, benchmark datasets, and sensitivity matrices are included in the full institutional edition.

The complete technical report — including cumulative curves, annual revenue tables, cost recovery bank evolution, benchmark comparison datasets, NPV tables, and oil price sensitivity outputs — is available and for sale as a professional publication.

4. Cumulative & Discounted Outcomes

- Cumulative Public Sector (2028–2053): US$ 23.5B

- NPV10 Public Cash (real): consistent with ~73% net value share under proxy assumptions

Undiscounted totals illustrate aggregate fiscal magnitude; NPV10 contextualizes time-value effects relevant for sovereign planning.

5. Oil Price Sensitivity (Real USD)

- $60 Brent – Reduced public share, still investable

- $70 Brent – Base case

- $85 Brent – Increased progressivity via R-factor

The fiscal structure demonstrates structural progressivity as profitability increases.

6. IMF-Style Technical Audit Sweep

- Production life verified (2028–2053)

- Cost recovery bank reconciled annually

- No double counting of fiscal streams

- NPV10 consistently discounted (10% real)

- Benchmark applied under identical economic base

- All calculations reproducible

Within modelling constraints and publicly available structural parameters, the framework is internally coherent and institutionally defensible.

7. Global Fiscal Context

PSCs worldwide share core elements: royalty, cost recovery, profit oil allocation, and frequently progressivity. Differences reflect basin maturity and negotiation context.

Suriname’s Model PSC incorporates royalty, capped cost recovery, profitability-linked R-factor progressivity, state participation, and conventional taxation — a structure consistent with modern institutional fiscal design.1–3

Comparisons with neighboring jurisdictions such as Guyana should be interpreted within their respective historical and geological contexts.

The author participated, within a broader multi-stakeholder technical process around 2010, in discussions contributing to the refinement of Suriname’s PSC framework.

Selected Institutional References

1 IMF – Fiscal Regimes for Extractive Industries.

2 World Bank – Extractive Industries Sourcebook.

3 AIEN – Model Petroleum Agreements & Negotiation Principles.

8. Concluding Observations

- Gran Morgu is a long-cycle offshore development.

- Fiscal outcomes depend materially on price and cost performance.

- The proxy PSC framework indicates structurally progressive characteristics.

- This report is analytical and non-political in intent.

About the Author

Marcel Chin-A-Lien

Global Petroleum & Energy Advisor

Nearly five decades of international upstream experience integrating exploration geology, fiscal modelling, PSC design, M&A evaluation, and negotiation advisory.

- Drs. Petroleum Geology

- Engineering Geologist – Petroleum Geology

- Executive MBA – International Business (Petroleum & M&A)

- MSc – International Management (Petroleum Focus)

- Certified Petroleum Geologist #5201 – AAPG

- Chartered European Geologist #92 – EFG

Email: marcelchinalien@gmail.com

Professional Safeguard Statement

This document reflects independent modelling and professional opinion only. Official contractual interpretation must rely on legally binding documents. All numerical outputs may change if input parameters are modified. © Marcel Chin-A-Lien — Petroleum & Energy Advisor (Independent).